Jan Rispens, head of the Renewable Energy Hamburg Cluster (EEHH), looks ahead to the Hydrogen Technology World Expo in Hamburg and discusses how the hydrogen ramp-up could be accelerated.

Interview by Monika Rößiger

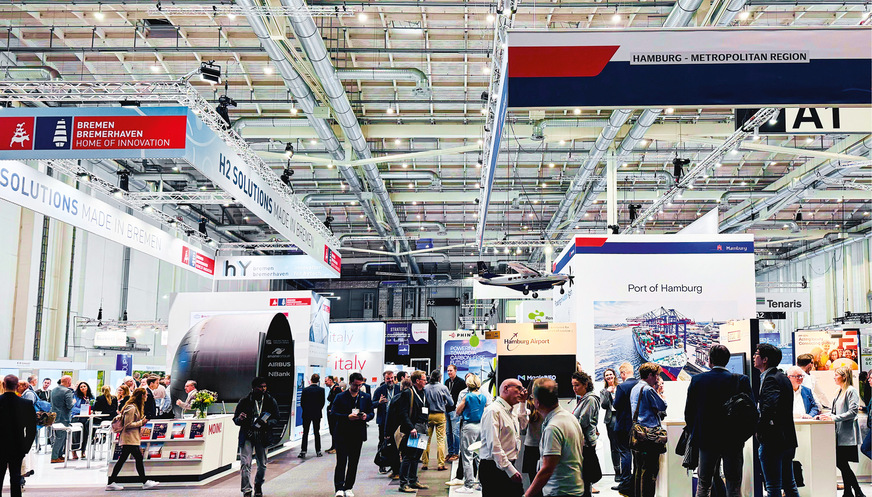

H2international: The “Hydrogen Technology World Expo” will take place in Hamburg from October 21 to 23. The hydrogen trade fair was already a great success in 2024. And this year, it appears there will be even more participants?

Jan Rispens: Yes, the rented exhibition space alone is 30 percent larger this year than before. And the number of exhibitors has also increased significantly. So there is a great deal of interest in taking part in this trade fair. It has also been extended from two to three days, because two days were simply too short. In this respect, the Hydrogen Technology World Expo will be a leading trade fair for Europe. And, I believe, also worldwide.

What can we expect?

What we will definitely see at this trade fair is that the technology has matured even further. Electrolysers, compressors, storage systems – in other words, technical development is progressing.

What might be different from last year?

I think the wheat has been further separated from the chaff. There may be less euphoria, but in return more real orders and contracts.

Now, Hamburg is not the only location for hydrogen trade fairs. How does the Hanseatic city compare internationally, for example with Rotterdam?

Yes, there are other trade fairs and events. There is also the European Hydrogen Week in Brussels. But I believe the trade fair with the highest technology content is the Hydrogen Technology World Expo in Hamburg. It showcases concentrated German technological expertise, plus European and international know-how.

What else does Hamburg have to offer in terms of hydrogen and renewable energy, apart from being a trade fair location?

Hamburg is firmly committed to becoming a hub for green hydrogen. Both for the production of green hydrogen and for its import. This naturally includes the expansion of renewable energies. For a city-state, Hamburg is very ambitious in this area, I think. For example, the Hanseatic city is developing wind farms on its own land, such as in the port or in the outskirts. So there is a lot of ambition behind it, even if this is only possible on a smaller scale in a city-state compared to a territorial state.

What are the plans of the newly elected Senate in Hamburg, consisting of Social Democrats and the Green Party, for the energy transition?

Hamburg aims to become much better in the field of solar energy than in the past. The city administration also says it wants to work with businesses, industry and the housing sector to install significantly more solar modules than in recent years. I believe something is starting to move here.

And in the hydrogen sector?

The goal of decarbonising industry with green hydrogen is also being pursued further, and the ambition remains strong. Hamburg is also providing substantial financial support for this. For example, for the IPCEI projects aimed at building a green hydrogen economy, Hamburg is contributing around EUR 220 million in funding, in addition to federal funds.

What exactly is planned and how is it to be implemented?

This is being driven primarily by the municipal companies Hamburger Energiewerke and Hamburger Energienetze. They are 100 percent owned by the city. Hamburger Energiewerke is developing a 100 megawatt electrolyser at the Moorburg site together with the company Luxcara. Hamburger Energienetze is building a 40-kilometre pipeline network to transport hydrogen to key energy customers in the port.

The government is also supporting the private sector in switching to hydrogen. For example, the operators of tank farms and terminals, to enable the import of green fuels. There is currently an application for approval of an ammonia terminal. A positive decision is expected soon. In addition, work has begun to convert tanks currently storing fossil oil into methanol tanks. The city is supporting this with fast-track approval procedures, and you can sense a high level of motivation from the administration. I would say Hamburg is doing everything it can to enable the import of green hydrogen and green fuels into Germany.

Let’s turn to federal policy: There is no clear course on hydrogen. And the rapid expansion of renewables is even being called into question – what can we expect?

On the one hand, I can understand that a new government wants to take stock of the finances first. On the other hand, it must be said that the rapid expansion of renewables is essentially a no-regret measure. There’s not much you can do wrong. Even if the expansion targets are reached earlier. On the contrary, that would only be beneficial, especially with regard to hydrogen. However, the whole process could perhaps be made more cost-efficient.

In what respect?

In terms of infrastructure. If the expansion of infrastructure is slowed down now and it later turns out that the infrastructure is fully utilised and many green electricity suppliers have to be curtailed – that can no longer be corrected in the short term. That’s why I believe we must not lose momentum in expanding infrastructure. This applies to electricity grids as well as to the emerging hydrogen networks. Today, we are unfortunately losing a lot of valuable green electricity because the power lines to southern Germany are overloaded and cannot be built quickly enough.

Then there’s the discussion about gas-fired power plants. Should they initially run on natural gas or be hydrogen-ready from the start?

The most important thing is that we get a decision on gas-fired power plants quickly. We want to shut down coal-fired power plants with a total capacity of 30 gigawatts. Once they are gone, we need a replacement for dark doldrums, especially in winter. As the EEHH Cluster, we would prefer to have highly flexible gas-fired power plants that we initially operate with natural gas and later gradually with hydrogen.

“Hourly balancing and additionality make hydrogen 50 percent more expensive than necessary.”

Do we need 20 gigawatts, or could the coal-fired power plants be replaced with less capacity?

Twenty gigawatts is, I think, quite a lot, but I consider ten gigawatts to be quite appropriate. That was also the plan of the current coalition government, which applied to the European Commission in Brussels for state aid approval. The framework conditions for the power plants should now be created quickly. In my view, most companies that will build these gas-fired power plants are likely to be interested in making them H2-ready. Otherwise, they would have a “stranded investment” in ten or twenty years. So they will make sure to build a gas-fired power plant that can later be operated with hydrogen in various blending ratios. Perhaps even up to one hundred percent hydrogen.

What is the current state of the technology?

Well, turbines are already available at the prototype stage, both in Japan and in Germany. For all gas-fired power plants currently being planned, investors are considering how the plants can be operated in ten or twenty years and whether that will also work with hydrogen. This also applies to the gas and steam turbine plant being built by Hamburger Energiewerke on the Elbe island of Dradenau.

Nevertheless, there is currently a sense that the hydrogen ramp-up is stalling. Projects are being postponed or cancelled altogether. What could be the reason?

The main problem is the Delegated Act of the European Union, the RED II and III directives, which aim to introduce hourly balancing relatively quickly. In order to balance the electricity from wind farms or solar plants on an hourly basis, this electricity must also be purchased via PPAs. Until 2030, monthly balancing is still permitted. But since most projects are unlikely to be completed before 2030, they will immediately fall under the hourly balancing requirement.

That means that …?

… much larger quantities of green electricity must be purchased than with monthly balancing, in order to cover the demand for electrolysis at all times on an hourly basis. Green electricity purchased long-term via PPAs with guarantees of origin is relatively expensive. The hourly balancing requirement from 2030 therefore makes the hydrogen produced even more expensive.

There is also a second criterion, the so-called additionality. Another obstacle?

Yes, because it means that I may only use electricity from new wind farms or new solar plants for electrolysis. But the market for new wind farms and solar plants is complicated. I would have a much wider choice if I could source electricity from all green power providers. That is, from both old and new renewable energy plants. That would be significantly cheaper. Many old wind farms no longer receive EEG subsidies and their operators are offering their electricity on the market. But due to the additionality requirement, electrolysis operators cannot use this offer.

“The additionality requirement could be abolished entirely. Why should an electrolyser only be allowed to use electricity from new wind and solar farms? That makes no sense at all!”

These are two major obstacles to the hydrogen ramp-up?

Absolutely. Hourly balancing and additionality make hydrogen about 50 percent more expensive than necessary. An industrial company that wants to decarbonise its production using green hydrogen is already facing the challenge that this is two to five times more expensive than hydrogen from natural gas. And if hydrogen becomes another 50 percent more expensive due to these two regulations, that is an extreme investment barrier. This is also the main reason why many potential buyers are not investing now, but waiting.

But these regulatory brakes could be removed relatively easily, couldn’t they?

Definitely! The additionality requirement could be abolished entirely. Why should an electrolyser only be allowed to use electricity from new wind and solar farms? That makes no sense at all and does not apply to EV charging stations, data centres or any other sector of the economy. So why only for electrolysers? I see no ecological benefit in it.

There is another reason why I would abolish it. If the European countries achieve their expansion targets for renewable energy, the share of renewables in the electricity mix will already exceed 80 percent by 2030. Then additionality no longer matters, because the CO2 intensity of the electricity will have become very low. As for hourly balancing, we should therefore extend the deadlines to 2035 or even later. That means monthly balancing should be allowed until at least 2035. By that time, the share of renewable energy in the electricity sector in the EU will already be very high. In Germany, it is even expected to reach 100 percent. For an electrolyser operator, it will then no longer matter whether balancing is done monthly or hourly, and whether the electricity comes from old or new wind or solar plants. In this respect, this solution would be simple and ecologically justifiable in my view. But this also requires recognition in Brussels that with the current overly rigid regulation, the EU will be in a pretty poor position in terms of the hydrogen ramp-up by 2030.

About Jan Rispens

Since 2010, Jan Rispens has headed the Renewable Energy Hamburg Cluster (EEHH), an industry network in the Hamburg metropolitan region with around 300 companies and institutes. Since 2021, EEHH has been building its own cluster segment for the hydrogen economy, which now has around 80 members. Jan Rispens, born in the Netherlands, where he completed a degree in electrical engineering, previously worked for Greenpeace Germany and the German Energy Agency. From 2002 to 2010, he served as managing director of the Wind Energy Agency Bremerhaven/Bremen e.V. (WAB). He is a member of the advisory board of the “Hydrogen Technology World Expo”.

About the “Hydrogen Technology World Expo” 2025 in Hamburg

The hydrogen trade fair in Hamburg already attracted great interest last year.

More than 1,000 companies, 20,000 participants and 300 speakers have registered this year for what is, according to the organisers, “the world’s largest supplier trade fair for hydrogen technologies”. Exhibitors and speakers will present technical solutions, production facilities, components and innovative materials along the entire hydrogen value chain. From production to application in mobile or stationary systems, transport and storage. Manufacturers of electrolysers, fuel cells and CO2-neutral fuels will offer their expertise for infrastructure and services.