Electrolysers are predestined for local flexibility markets: as is well known, they can adjust their power consumption at short notice, alleviate grid congestion and at the same time convert surplus wind and solar power into green hydrogen. However, this potential remains largely unused in Germany to date. While other countries have already transferred local flexibility markets into regular operation, Germany continues to rely on cost-based redispatch, thereby also slowing down the ramp-up of the hydrogen economy.

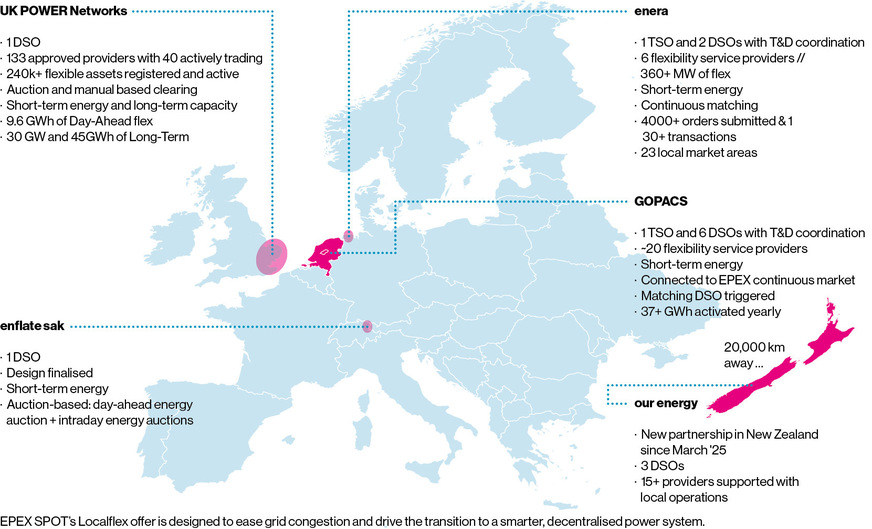

Germany itself co-developed local flexibility markets and technically tested them in pilot projects such as enera. Internationally, these approaches attracted considerable attention. Other countries have since gone a step further. In Great Britain or the Netherlands, local flexibility markets are already part of the regular toolkit of grid operators. Germany, by contrast, continues to rely primarily on cost-based redispatch. As a result, large parts of the decentralized flexibility potential remain unused, precisely those resources that would be crucial for a successful energy transition and an economically viable hydrogen ramp-up.

The paradoxical reality

Modern grid regulation can create incentives to resolve grid congestion efficiently via the market: Great Britain links investment and operating expenditures in the so-called TOTEX approach, enabling grid operators to use market-based flexibility instead of new lines. There, this is already established practice, for example at UK Power Networks DSO, where since 2024 a flexibility market with hundreds of thousands of flexible assets and dozens of active providers has been operating.

Although congestion management and grid expansion face enormous challenges, valuable demand-side flexibilities remain unused in Germany, precisely the resources needed for a successful energy transition. This also applies to offshore electrolysis: while combined electricity-hydrogen connections would be technically possible in the North Sea, German regulations prevent their grid-supportive integration. Energy generated from offshore wind is therefore often curtailed.

Local flexibility markets are intended to resolve grid congestion via a market- based approach. Grid operators procure flexibility in a targeted manner, for example from batteries, power-to-X, industrial plants or electrolysers. Operators can offer their capacity specifically where it can be used in a grid-supportive way.

Via platforms such as EPEX Localflex, flexibility supply and demand are brought together in clearly defined zones, usually via auctions. In this way, grid-supportive behavior is remunerated, congestion is avoided and grid expansion can be reduced. This market-oriented procurement creates a transparent, non-discriminatory mechanism that enables new business models and significantly accelerates the integration of decentralized flexibilities.

The hurdles in Germany’s regulatory framework

Policymakers have created this status quo, and they can also change it. Article 13a of the German Energy Industry Act (EnWG) effectively cements cost-based redispatch as the standard. Instead of fully implementing the European Clean Energy Package, Germany has taken a special path here. Article 14c EnWG could enable market-based procurement of flexibility by distribution system operators, but remains unused to date, so that genuine congestion management via the market is effectively absent.

In addition, the Incentive Regulation Ordinance (ARegV) does not recognize the costs of market-based flexibility procurement, a clear disincentive that pushes grid operators toward CAPEX-intensive “fit & forget”. Finally, excessive concerns about IncDec gaming are slowing the discussion, although proven countermeasures exist.

Immense savings possible

Local flexibility markets activate resources that hardly appear in Redispatch 2.0 so far: heat pumps, charging infrastructure, industrial loads, smaller generators, and above all electrolysers as electricity consumers for hydrogen production. Instead of curtailing wind farms and paying power plants for redispatch, grid operators could activate flexible consumers in a targeted way. Studies and practical experience show that grid expansion costs would decrease significantly; in Great Britain, targeted savings of hundreds of millions are reported.

The magnitude of possible savings would also be considerable in Germany: a study by Frontier Economics commissioned by AquaVentus shows that integrating offshore electrolysers and hydrogen pipelines can reduce system costs in the German energy system by up to 1.7 billion euros annually (see H2international 5-2025). These estimates refer only to one type of flexible generator, namely offshore hydrogen. The overall potential increases sharply with the diversity of technologies, as power-to-X plants, heat pumps, EV fleets, battery storage, etc. are also included in the market design.

It is also crucial that flexibility markets complement the wholesale market; they are not a parallel universe. They enable close coordination between transmission system operators and distribution system operators and create transparency, competition and reliable price signals for investments in flexibility, a lever that is particularly important for business models in the hydrogen sector. And: they are EU-compatible. The upcoming European “Network Code on Demand Response” anchors local flexibility markets as a standard instrument for congestion management in Europe, a new opportunity for Germany to catch up internationally.

What this means for the H2 ramp-up

Electrolysers will play an important and fundamental role here; especially those producing hydrogen at sea. Unlike onshore plants, offshore electrolysers do not compete with grid connections but complement them. When the wind blows strongly and grid congestion looms, offshore electrolysers convert electricity into hydrogen, which is transported via dedicated pipelines. This relieves expensive subsea cables and avoids curtailment.

In addition, this approach allows sectors to be linked, from electricity to heat to mobility. The revenues generated in the process improve economic viability. Where grid congestion currently delays H2 projects, flexibility markets can facilitate location decisions: they provide a price signal indicating where and when flexibility is particularly valuable and help integrate electrolysis clusters in a system-supportive manner. For operators, this creates a dual benefit: participation in the wholesale market and additional regional flexibility remuneration, both within clear, rule-based processes.

© epexspot / NEONBOLD

Further development instead of system disruption

No one is calling for the abolition of cost-based redispatch overnight. What is needed is a hybrid model: the existing redispatch remains in place for large generation plants, complemented by market-based procurement for demand-side flexibility and smaller assets. In parallel, three regulatory building blocks are crucial:

1) Reform Article 14c EnWG and explicitly extend the term “flexibility services” to congestion management; missing specifications for distribution system operators are to be developed jointly.

2) Recognize flexibility costs: classify flexibility procurement as permanently non-controllable costs in incentive regulation, only then will a fair investment and operating incentive emerge.

3) Standardize processes: uniform prequalification, market-neutral baselines, transparent clearing rules and coordinated interfaces between TSOs and DSOs.

This creates a scalable model that transfers pilot knowledge into regular operation, compatible with European regulation, connectable for the energy industry and attractive for new flexibility investments.

IncDec gaming? Manageable and overestimated

Concern about strategic bidding behavior, so-called gaming, must be taken seriously, but must not block progress. Practice, including in German pilots, shows: gate-closure rules, robust baseline methods, price caps and market monitoring are effective. In addition, small, shiftable loads such as heat pumps or many charging processes are only partially suitable for gaming; the technical effort is disproportionate to the potential return, especially as the risk of detection is high. The measurable benefits of local flexibility markets, less grid congestion, lower expansion costs, faster hydrogen ramp-up, clearly outweigh the theoretical risk. The right answer is therefore good market design, not abandoning markets.

A German comeback, now

Germany co-developed an innovative concept and tested it in its own energy system. Other countries have transferred it into regular operation; we can do the same. Anyone who blocks local flexibility markets blocks cost efficiency in grid expansion and the flexibilization of our power system, and thus the H2 ramp-up. Policymakers must set the right course: if regulation and market design are considered together, Germany will unlock its flexibility potential, reduce system costs, scale innovation and accelerate the energy transition. Local flexibility markets could provide exactly this lever. Without them, a large part of flexibility in the energy system remains unused, and with it part of the hydrogen potential.