© wallstreet-online.de

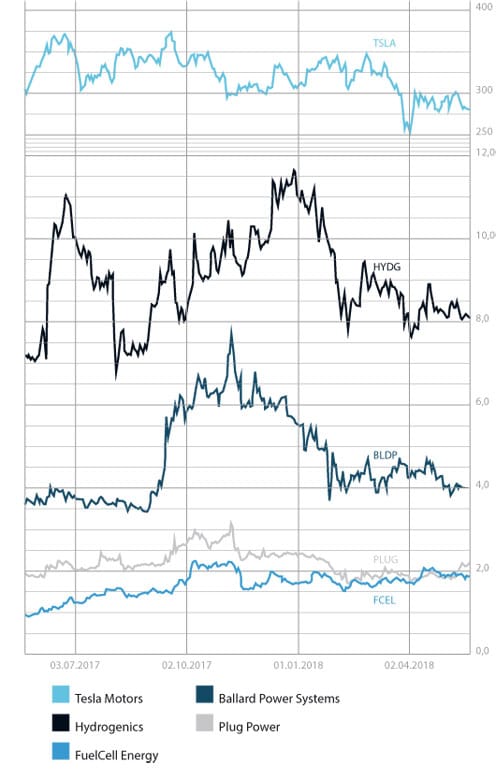

Like Canadian competitor Ballard, Hydrogenics (Nasdaq: HYGS) has made investments in several markets, most of all, China, where demand for fuel cells is projected to rise. Both have entered into agreements with Alstom and Siemens. That the latter two have founded a joint venture to merge their railroad divisions suggests to me that keeping two experienced suppliers on board is part of their failsafe system. Ballard has also partnered with China’s CRRC, the world’s largest rolling stock manufacturer. And, like Hydrogenics, it is upgrading locomotives and trucks, replacing diesel with hydrogen fuel. In short, a healthy dose of competition never hurt anyone. Both companies have proved why they’re the crème de la crème of the fuel cell industry and that they are operating on high-growth markets. Besides China, India is shaping up to be a promising candidate for expansion. Plus, and in contrast to Ballard, Hydrogenics has a strong electrolyzer business.

On to the results. The first quarter brought in USD 8.1 million in revenue, compared to USD 8.7 million one year ago. Net loss improved and was below USD 2 million, or USD 0.13 per share, whereas cash reserves amounted to USD 19.4 million. Backlog exceeded USD 140 million. Daryl Wilson, Hydrogenics’ chief executive, regarded the first quarter results as “not reflective of the potential for top line expansion this year and beyond.” With a temporary price drop behind us, now is a good time to buy Hydrogenics stock to cushion a well-diversified fuel cell portfolio that promises medium-term gains.

Risk warning

Share trading can result in a total loss of your investment. Consider spreading the risk as a sensible precaution. The fuel cell companies mentioned in this article are small and mid-cap ones, i.e., they may experience high stock volatility. This article is not to be taken as a recommendation of what shares to buy or sell – it comes without any explicit or implicit guarantee or warranty. All information is based on publicly available sources and the content of this article reflects the author’s opinion only. This article focuses on mid-term and long-term prospects and not short-term profit. The author may own shares in any of the companies mentioned in it.

Written by Sven Jösting

0 Comments