Setting up various production lines for stacks is at the focus for Ballard Power. With these, the company can act and deliver during the ramp-up in the next years. With still nearly 800 million USD in the bank, Ballard is in a comfortable situation and is able to finance all investments from its own resources. That the company is valued at the stock exchange with only about one billion USD seems incomprehensible in view of the prospects.

Strategically interested companies could and should seize the opportunity and get on board with Ballard stock as long as the stock market valuation is so low. What if a Mr. Adani were to come knocking again? Or automotive suppliers such as Dana, Tyco or Magna? Anything is possible. The only protection against this: significantly higher share prices, so a stock market valuation that matches the future prospects.

Advertisements

Figures have little informative value

Current sales will be dramatically exceeded in the coming years, when the ramp-up of the FC markets for commercial vehicles of all kinds, ships and rail vehicles begins. In this respect, the quarterly losses in 2023 and 2024 are due to high R&D expenses and the expansion of capacity and have little to no meaning. What if in a few years’ time instead of the still scant individual orders of 50, 100, 200 FC modules per year, 1,000, 5,000, 10,000 and more FC modules were to be delivered – and for each individual market? Then Ballard would have the necessary capacities and could deliver.

Opening of the Still’s FC production site in location Hamburg

The forklift truck manufacturer Still (subsidiary of Kion, majority-held and part of the Chinese Weichai Group – which in turn holds about 15 percent in Ballard Power) is relying on the FC stacks from Ballard Power. On November 10, 2023 in Hamburg, the ceremonial opening of the first production line for 24-volt fuel cell systems took place. In the future, 4,000 FC forklifts will roll off the production line there every year.

7-billion-dollar hydrogen hub plan

Ballard benefits indirectly from the planned establishment of a US-wide network of seven hydrogen production centers (hydrogen hubs). This is because the widespread production of green hydrogen is a great opportunity for many – and even more so in the future – Ballard customers to invest in products that can use hydrogen: shipping companies, trucks, buses, ships, rail vehicles and many more. In six of the seven hubs, Ballard sees the perfect positioning for itself and its customers in hydrogen and fuel cells.

Forsee Power proves to be a stroke of luck

If you look at the current figures of the French battery manufacturer Forsee Power, you have to give Ballard credit for a good hand with the investment – Ballard is one of the largest single shareholders. A massive 83 percent increase in turnover in the third quarter to 47.9 million EUR. In the first nine months, that amounts to a plus of 67.6 percent to 126.6 million EUR. For the whole year, it is to be 160 million EUR, then 235 million EUR in 2024, and 850 million EUR turnover in 2028 is the goal.

The two companies work perfectly together, as the batteries from Forsee are put to use in, among other things, the FC systems of buses and Ballard customers. Forsee at around 2.50 EUR per share seems to me to be a good buy if you want to have batteries in your portfolio and see it as a complement to the fuel cell.

Solaris is the perfect forerunner

The Polish bus manufacturer Solaris is continuously ordering more FC modules from Ballard, 350 in total this year alone – another 62 were recently added. Since Ballard supplies various bus manufacturers as a partner for the fuel cell, Solaris is a very good example. This market is only at its start, and Ballard as number one and frontrunner already has experience of over 100 million kilometers traveled. The newsletter Information Trends see the market for FC long-haul buses in general as one of the fastest growing hydrogen markets.

In the next 15 years, globally over 73.4 billion USD are to be invested in new FC buses. The forerunner is China. FC buses are becoming increasingly cheaper, even if they’re still more expensive than pure battery-electric buses. Convincing here are the arguments of range and time or type of refueling. Parallel to this, the H2 infrastructure is being established. Consider this: Ballard has more than ten big bus manufacturers that exclusively rely on fuel cells from Ballard. In China, Ballard via a joint venture with Weichai Power is also the supplier for various bus manufacturers there – that is only one of the over 30 platform partnerships. Currently, there are tenders for over 17,000 buses worldwide.

Individual orders increasingly larger

Randy MacEwen as CEO has said: from small series occurs the ramp-up to large series. From batch sizes of 10 to 100, there are now massive numbers. The same goes for many other markets: The rail vehicle manufacturer Stadler reports that they are waiting for the acceptance for 25 hydrogen-powered trains, after having already received a firm order for four such trains in California.

In trucks, OEM partners such as the German company Quantron rely on Ballard: Among other things, they deliver hydrogen-powered small trucks Ikea. The platform partnership with Ford for the F-Max raises great expectations: What would it mean if Ballard were to supply FC modules for over 10,000 trucks per year? It is important to be, like Ballard, a technology leader and also have the ability to deliver (capacities).

My only concern: What happens when a big player in the market takes advantage of the situation and makes Ballard a takeover offer – like Cummins has done with Hydrogenics? A participation in a strategic partnership would be a share price turbo, though.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Written by Sven Jösting, December 15th, 2023

In the past weeks, news reached us from The Central Country: China is repositioning itself in the field of hydrogen and intends to take the lead in various fuel cell and hydrogen markets around the world. When it came to the solar and wind energy sectors, or even battery-electric mobility, China stimulated them with its extensive subsidy programs and the People’s Republic quickly advanced to the position of global market leader. Will we now see the same development in the H2 and FC sectors?

Advertisements

First, China defined, among other things through the CO2 footprint, the various colors of hydrogen for itself at the end of July and then, August 8, through six central authorities (standardization administration, NDRC, ministry of industry and information technology, ministry of emergency management and national energy administration), set corresponding guidelines. According to the Formation Guidance for Standard System of Hydrogen Industry, standards for the use of hydrogen in various markets and application fields are to be established by year 2025. This covers the various production processes of hydrogen, safety aspects, storage and transport, H2 infrastructure and various fields of application/markets.

This can safely be viewed as a framework in which the Chinese government could soon launch support programs for companies, provinces, universities and research institutes on a grand scale. Perhaps as early as 2024? For three years, we’ve been waiting for such a program – one with a volume that could be comparable to the US Inflation Reduction Act (500 billion USD, a trillion even?).

As China has major problems in the infrastructure/construction sector, the swing in the direction of hydrogen and climate protection could represent the perfect counter: growth through sustainability. This should now become a reality in one to two years. China has long been by far the world’s largest producer and also consumer of hydrogen (natural gas-based). In the future, the hydrogen is to eventually become green, even if surely also the color blue (natural gas reforming with CCS) is used in the transition.

What does this have to do with the H2/FC shares discussed here?

China will be setting down specifications that will influence the entire H2 industry worldwide, is the expectation. The use of fuel cells in motor vehicles of various types (from commercial vehicles to passenger cars) could help this technology achieve a breakthrough, if for example a national quota were to be introduced like that previously made for battery-electric. The same goes for the corresponding infrastructure and, of course, also production, storage and transport.

Based on planning until now, China was to have 1 million vehicles with H2 drives on the road by year 2030. A suitable funding program could ensure that it becomes many millions. For comparison: South Korea plans to have around 6.1 million FC vehicles on its roads by 2040.

For such a ramp-up, many companies active in this field in China need to prepare themselves. Toyota and Hyundai, but also Ballard, Cummins and Bosch, with large investments in regional production facilities for among other things FC stacks, are already in position. It is only a question of time when the global industry of suppliers show their commitment here.

On the small scale, this can already be seen in individual provinces and major cities: Shanghai plans by year 2025 to build up the number of H2 refueling stations from the current 14 to 70 and the number of FC vehicles from today’s 2,500 to 10,000 (primarily buses and commercial vehicles). This allows the conclusion that Shanghai wants to be prepared for the plans (subsidies) of the central government.

Why is the year 2023 the start of the hydrogen megatrend?

Trend research is showing green – including with hydrogen. John Naisbitt in his bestseller “Megatrends” has shown through many examples that the number 20 has a special meaning. And exactly 20 years ago, in 2003, the book “The Hydrogen Economy: The Creation of the Worldwide Energy Web…” of visionary Jeremy Rifkin was published in German (the English edition a year before in 2002). After reading it, you’ll know what is possible in terms of hydrogen.

Today, it is real. The book was my entrée into this subject area. From trend research, we know that for a new megatrend to go from its starting to melting point, it takes an average of 20 years. We’re penning the year 2023. The stock market is in the starting blocks. Will Naisbitt and Rifkin be right? Looks that way.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

That the wind subsidiary Siemens Gamesa will still cost its parent company a lot of money has been the case for a while. Too great are the problems with some wind turbine types (onshore), and integration also costs money until synergies properly take effect and cost reduction potentials can be leveraged. Siemens Energy itself still see financial risks with this in the area of 1.5 to 1.7 billion EUR. It could, at the end of the day, as well be two billion. Provisions amounting to 1.6 billion EUR have already been set aside for this purpose, which will come into use in the coming two years. The second quarter brought an overall loss of 2.9 billion EUR (minus of 4.5 billion EUR for the entire year is expected). That’s as far as the negative news.

The good news: Siemens Energy will well be able to cover these losses (liquidity at over 4 billion EUR), even if this will have a very negative impact on the overall result for the current fiscal year and it could take one to two years to return to positive figures. Look at the bigger picture: The order intake worth tens of billions is reason to celebrate. In addition, the risk has now been named, so the stock market will be able to include this in its investment decisions. Investors with time to allow should profit from the turnaround through again rising share prices.

Advertisements

The stock market adage “buy on bad news” is the perfect as a basis for the invest in Siemens Energy. Because Siemens Energy with an order volume of over 110 billion EUR is virtually flooded with orders relating to energy security, hydrogen and the like, but there are not many companies in the world that as a one-stop shopping partner are able to offer everything from a single source. Many of the business units are doing very well and are highly profitable.

If the share price weakens further, 13 or even 12 EUR would be the perfect entry price as well as usable for the price reduction of old stocks. In two years, I expect prices of over 30 EUR.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

My recommendation to use the temporarily very weak prices in Cummins for continued and new buys has already paid off: The share price grew from around 200 to over 255 USD. And it will continue to, even though Cummins is increasingly focusing on new markets like hydrogen (engines, electrolysis, stacks for commercial vehicles, etc. – we reported).

Cummins can finance its own growth well from its own means through corporate earnings. On average, 34 percent of corporate profits are distributed to shareholders as dividends – in 2022, it was 6.28 USD per share. This was topped up by seven percent on July 11 to 1.68 USD per share for the quarter. The company’s growth rate of 26 percent per year on average over the past five years is solid. Cummins now sees turnover in the current fiscal year at 33 billion USD and expects an earnings per share of 19.80 USD, which corresponds to a growth of 31 percent. A good justification for further rising prices.

Advertisements

Share price decline despite good figures

Cummins reports for the second quarter a turnover of 8.6 billion USD (plus of 31 percent) and profit of 720 million USD, which came out lower than expected, however, and allowed the share price to sink from over 255 USD to 230 USD – thus already back to buy level, as the guidelines are unchanged.

Together with Air Liquide, Cummins Engine acquired Canadian company Hydrogenics in 2019 for 290 million USD. In the transaction, Air Liquide retained at that time a 19 percent share in the company. This share Air Liquide has now sold to Cummins for the equivalent of about 156.5 million USD, making the value of Hydrogenics as per today the equivalent of over 823.7 million USD. Cummins plans with subsidiary Accelera, in which Hydrogenics is consolidated, to build an annual electrolysis capacity of 3.5 GW in the next years. A diversity of large orders – 500 MW in China, 500 MW in the USA, 500 MW in Spain and 1 GW in Belgium – are already in the books of Cummins or Accelera.

Considering that Plug Power intends to build 5 GW of electrolysis capacity within a few years and is currently valued on the stock exchange with a good 6 billion USD, Cummins should consider placing its subsidiary on the stock exchange, possibly while also retaining a majority shareholding, like Thyssenkrupp did with Nucera. The consequence in this purely theoretical consideration: Capital inflow of over 2 billion USD, with which, on the one hand, the price for buying Hydrogenics is covered (flows back in); in addition, an extraordinary profit beckons; and thirdly, Accelera via the stock exchange would receive new growth capital (for acquisitions?) – just as a thought experiment.

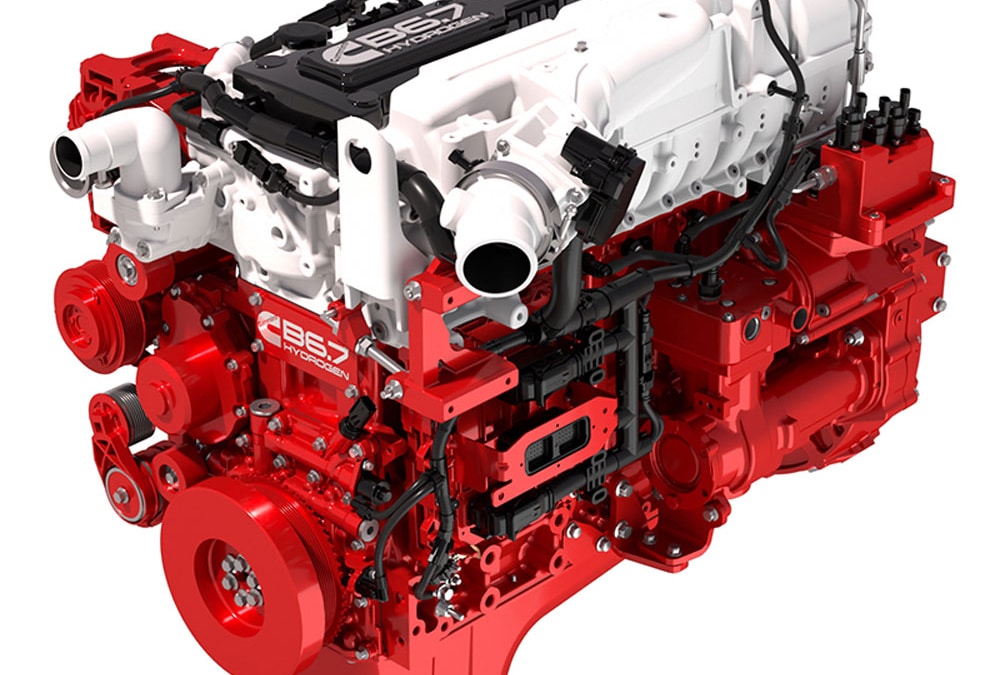

Hydrogen-powered engines

The automotive expert journal WardsAuto reports on how advanced Cummins is in its work to bring engines to market that run on hydrogen. There is to be a new version of the successful B6.7 diesel engine that with its powertrain burns hydrogen and can be used in heavy trucks. After all, there are already restrictions in place in California that prohibit already starting 2024 the operation of diesel trucks on, among other places, port grounds. Vehicles produced before 2010 will soon no longer be allowed on the roads of this state. A winning pass to all manufacturers of alternative drives – so employment of the fuel cell or direct injection of hydrogen as well as battery-electric systems.

With this, the new B6.7H 6.7-liter hydrogen engine (range of 483 km, or 300 mi) can quickly become a slam dunk if hydrogen and the corresponding infrastructure are available. So it is very suitable that the US government via the Inflation Reduction Act has provided 8 billion USD for the construction of six to ten H2 terminals distributed across the US – in addition to the many individual programs offered by states such as California.

Summary: Cummins Engine is working on a variety of platforms for the use of hydrogen in many applications such as heavy transport and rail but also for electrolysis, whether PEM or alkaline. The stock market will increasingly let this show in the company valuations. A real H2/FC blue chip is what Cummins has developed into.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

The press conference for the second quarter delivered a number of results that allow a very optimistic outlook for the future of the company. Ballard is positioning itself perfectly in its most important markets: buses and trucks, rail vehicles, maritime transport and stationary energy. This involves optimizing the production processes of all important components, cost reductions (scaling), local-for-local strategies (supply chains in the specific countries where Ballard maintains production) and ramp-up in the various regions of the world in which the company operates. A few examples:

In buses, the Canadian company is ahead of the pack in the fuel cell segment with a formidable market share of still over 70 percent. Recently, the largest single global order came in from customer Solaris for 96 FC buses (52 of them for public transport company Rebus in Güstrow near Rostock). In the next two years, it’ll be an astounding 10,000 FC buses (Europe and USA), a large share of which is sure to be Ballard. The USA is just beginning to pick up speed in this regard, and Ballard sees itself well placed to accept larger orders from, among other, New Flyer (have market share of about 66 percent in transit buses). Individual orders from municipalities have now grown from units of 1, 2, 5 to 100 FC buses.

Advertisements

The China card

In China, a lot is finally happening at the government level regarding hydrogen (see above). The chance of a comprehensive funding program starting in 2024/25 is increasing. Will China do it in dribs and drabs or, similar to the US government with the Inflation Reduction Act, launch a mammoth hydrogen program (investment incentives, subsidies for H2 production)? China could use hydrogen as a climate-friendly economic stimulus package for itself, given the current problems in the construction sector and with the infrastructure programs. In addition, new markets within electric transport can be established that could supplement or alternatively replace battery-electric ones, which would deliver a turbo boost to the world market for fuel cells.

For Ballard and its joint venture with Weichai (49:51), this allows a lot of possibility. CEO Randy MacEwen said: “We are believers in the long-term market opportunity for China. It is the largest market for production and use of hydrogen today and based on my recent visits there, I expect that to continue through 2030 – 2050. There is an enormous level of activity.”

Wisdom Motor sends 147 FC trucks to Australia

With Wisdom Motor – headquarters in province Fujian in China –Ballard has already started a strategic partnership in May 2022, which also includes the companies Templewater Group and Bravo Transportation (trucks and buses). Wisdom Motor in turn signed a cooperation agreement (MoU) with the Australian companies Pure Hydrogen and HDrive in November 2022, where Wisdom would supply over a five-year period 12,000 heavy-duty hydrogen-powered trucks (among them rubbish trucks).

Now, the first order has been completed, which entailed the delivery of 147 hydrogen-powered trash collection vehicles. Order value: 63 million USD. Supplier of the modules/stacks: The joint venture of Ballard and Weichai in China – exclusive even. Could this already mean that Ballard via the China JV is now supplying 2,400 FC modules per year here from this deal alone? The FC capacities of the JV currently correspond to 20,000 units per year, so this order is a very good start looking at the future.

Investments in China will be adjusted

Originally, Ballard wanted to establish its own MEA production with an investment volume of 130 million USD in China, among other things to counter import tariffs. This investment will be postponed for now, until there is clarity on the subsidy program. They are sticking to the plans, but don’t want to invest in land and all that until the FC market gets going there. However, they have concerning the supply chain all of the important connections already and can quickly act at the opportune time. To put it another way, this allows the interpretation that Ballard is first investing more in markets (USA, Europe) where the company expects to have better chances of winning orders in the near future. All this can also quickly be modified, however, if China accelerates its hydrogen strategy through subsidies and incentives.

Platform partnerships as a turbo

Ballard has been working for a long time on building so-called platform partnerships. This refers to customers who know how to use the fuel cell know-how (stacks & modules) for their own benefit and integrate this into their own hydrogen strategy, and acquire the FC modules exclusively from Ballard. They fully rely on Ballard in this regard and the company’s experience as well as the quality of its FC products. For Ballard, this means being able to deliver large quantities of modules/stacks to these partners in the future. In the bus sector, these are companies like Van Hool or Solaris, and with rail vehicles, Siemens Mobility and Stadler, to name a few examples. There could probably become 30 or more such partnerships, which means enormous and, above all, secure sales potential in the medium to long term.

Selection procedure of Ford speaks for Ballard

Ford Truck has decided, after comprehensive market analysis, to employ Ballard FC modules for its trucks of the F-MAX series. Two 120-kW FCmove XD modules be employed per truck. First, a letter of intent (LoI) was signed and the delivery of some modules for test purposes agreed on. From this will then come a large series. You can compare this with Bosch and Nikola, where Bosch supplies the FC modules.

This is an accolade for Ballard that underlines its expertise. Ford Truck builds, in addition to heavy trucks, many other vehicles such as construction vehicles and tractors that could in the future have Ballard inside. The truck production in Turkey is to be the first Ford site for this. Over 10,000 vehicles roll off the assembly line here every year.

Ford can itself install the Ballard modules perfectly on its own truck chassis, is the plan. It will surely take another year or two until, after test runs, the first large orders are given over to Ballard. The foundation, however, has now been laid. What would happen if Ballard were to supply 1,000, 5,000, 10,000 or more FC modules in a year – alone for this one platform partnership? According to Ballard: “As Ford’s fuel cell F-MAX truck platform matures, we anticipate this partnership to evolve into a long-term scaled-deployment-level module orders and supply arrangement.”

Canadian Pacific (CPKC) too has ordered for its production facility in Kansas City 20 FC modules for use in various locomotive types in order to gain experience from the test operation. They are also working together with railroad company CSX to make locomotives H2-ready or break away from diesel operation. A very large order can come out of this. Further orders are expected further in the course of 2023.

Figures

The reported loss for Ballard lay, as expected, at minus 0.10 USD per share for the quarter. The order volume rose strongly in terms of value to 147.5 million USD and will continue to do so. In the bank still lies a good 815 million USD in liquid assets. The ratio of sales development between the first and second half of the year is described as 30:70 percent, so the current second half of the year promises positive surprises regarding this. Really exciting will then be 2024/25.

Summary: The calm in the share price development of Ballard should end in 2024 at the latest and lead to a gradual rise in the share price that finds its foundations in the rising number of orders for the FC products in all the various platform partnerships, markets and regions. A turbo could be China, when clarity on subsidization is created. Therefore: Buy and leave alone. No hasty reactions. Think about Facebook, Amazon and Google in the first years: There were only “logical” huge losses – until the business models started to soar – the shares as well.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.