by Monika Roessiger | Apr 16, 2024 | Energy storage, Fuel cells, Germany, hydrogen development, international, News

Optimism at the H2 Forum in Berlin

A good 450 participants gathered at the specialist conference H2 Forum in Berlin February 19 and 20 to discuss innovative H2 technologies, strategies for the market ramp-up and the necessary regulatory framework conditions. A further 1,000 participants were connected online, even despite the considerable time difference in countries such as India and the USA.

The event was opened via a video by Kadri Simson, EU Commissioner for Energy. The two-day program was held under the motto “Empowering the future of hydrogen,” where this year’s focus was on the production of the green gas by electrolysis and its transport in Germany and Europe. At the H2 Forum were, among others, representatives from E.on, Enapter, EWE, Linde, FNB Gas and the H2Global Foundation. They discussed the role of hydrogen in the defossilization of the economic systems. Philipp Steinberg of the German economy ministry outlined the various phases of the development of the hydrogen core grid in Germany.

Advertisements

Feelings of optimism and assurance were tangible throughout the high-ceilinged rooms of the Estrel Congress Center (ECC) as players from politics, industry and the energy sector talked about ambitious H2 projects at home and abroad. Inspiring as well was the approval by the EU Commission a few days before of a series of IPCEI projects, thus ending for some participating companies years of waiting. Additionally, the carbon contracts for difference and the auctions of the European Hydrogen Bank are giving hope to business representatives.

Spain: Megawatt-electrolysis in practice

For example, Özlem Tosun, project manager for green hydrogen at Iberdrola Deutschland, reported on the experience with a 20‑MW electrolysis plant, making it currently the largest in Europe. “I hope it doesn’t stay that way,” she added, in view of the necessary market ramp-up for green hydrogen. The Spanish energy corporation, known in the country primarily as an operator of wind farms in the Baltic Sea, started operation of the plant in Puertollano, May 2022 in the presence of the King of Spain. The city with nearly 50,000 inhabitants is located about 250 kilometers south of Madrid. The electricity for the hydrogen production comes from a 100‑MW photovoltaic park a few kilometers away and flows via an underground cable into the production hall, in which 16 electrolyzers of 1.25 MW each perform their work. These produce annually up to 3,000 tonnes of green hydrogen, which is temporarily stored in tower-high pressure tanks at 60 bar. The electrolysis plant is located next to the fertilizer factory of Fertiberia and currently covers ten percent of their hydrogen requirement, which according to Iberdrola saves 48,000 metric tons of CO2.

“But this is just the beginning,” stressed Tosun. “In the coming years, Iberdrola wants to increase the production more than tenfold – to 40,000 tonnes by 2027.” The demand is there, since otherwise Fertiberia is using for its ammonia synthesis gray hydrogen obtained from natural gas. That no comparable plant for the production of green hydrogen on an industrial scale is yet in operation is also due to the fact that the whole thing is not as simple as it sounds in the big plans and letters of intent. “It didn’t go smoothly from the start,” admitted Özlem Tosun. “On the contrary – we had a lot of problems. But we also learned a lot and were able to improve a lot as a result. Not only technically, but also economically.” One of the most important points was to optimize the efficiency of electricity use. Contributing to this was that the performance and efficiency of the electrolyzers were able to be increased further and further.

Overall, the practical experience in Puertollano was important “to be able to scale the system.” As far as the large-scale production of climate-neutral energy sources is concerned, the multinational energy company not only sees itself as a pioneer, but is also optimistic about the future. Because Spain first wants to become independent of fossil fuel imports and then be able to export renewable energies. So it’s no wonder that Germany is for Iberdrola “a key market,” as Tosun says, “especially for green hydrogen.”

Lack of regulation as a stumbling block

How the development of a German and European hydrogen industry can be accelerated was one of many other topics discussed at the conference. It is important to break down barriers – for example lack of regulation and infrastructure – it was said in a panel discussion. Such hurdles, the speakers agreed, were in addition to the high costs for H2 production, like before, the crucial reasons why not a small number of companies, despite the positive feasibility studies, are still waiting with the final investment decision. The following figures show just how wide the gap is between aspiration and reality when it comes to the gas of the future: In recent years, the German government has raised the target for domestic production of green hydrogen from the original three gigawatts to ten gigawatts, yet so far not more than 62 MW of generation capacity has been installed. That there is a long way to go, but which can go faster, further practical examples have shown.

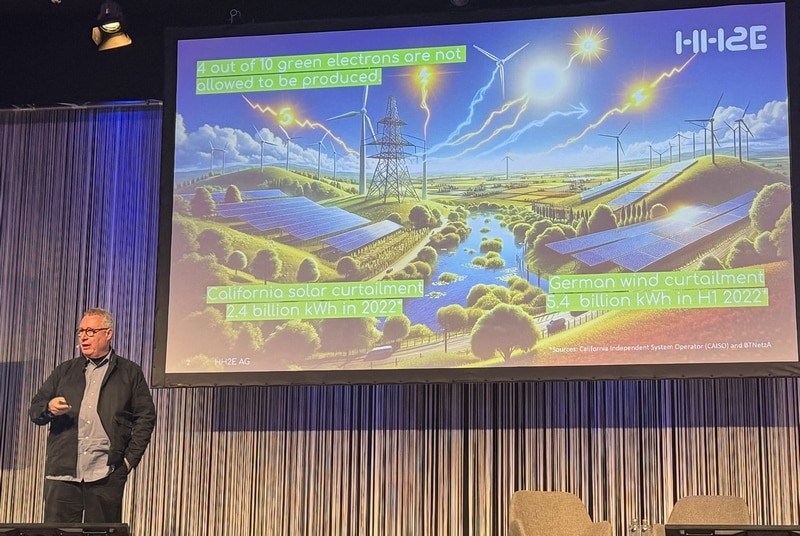

“Never waste a green electron again!”

“Did you know that with the wind power that was curtailed in the first half of 2022 alone 1.5 million households in Europe could have been supplied with electricity for a year?“ (The figure refers to average households with a consumption of 3,500 kWh per year.) That was one of several questions with which Alexander Voigt, managing director of HH2E, began his speech. “What could we do with all the green electrons that are not being generated only because the power grid cannot absorb them?” His answer, of course: Hydrogen! But also high-performance battery storage, to be able to offer energy for stabilization of the power grid. That’s how he explained the business model of the planned HH2E factory in Lubmin, Germany. It will use surplus electricity to “reliably and cost-effectively produce green hydrogen.” In addition will come CO2-free heating and, if required, the conversion of the “green molecules” back into electricity.

Alexander Voigt, CEO von HH2E, nutzt künftig Überschussstrom in Lubmin (Foto: Monika Rößiger), Source: Monika Rößiger

With this, the plant could contribute to the decarbonization of industry in Germany and, at the same time, support the energy supply. The final investment decision will be made shortly, according to Voigt, and then the way would be clear for the start of construction. In the year 2026, according to the plan, energy generation is to start: around 100 megawatts of total capacity in the first expansion stage, divided between a 56‑MW electrolyzer and a 40‑MW battery storage system. The electricity for electrolysis is coming from offshore wind farms in the Baltic Sea. Initially, the operators expect to produce around 7,200 tonnes of green hydrogen per year. The production capacity of the plant is scalable up to one gigawatt. Lubmin, once a transshipment point for Russian natural gas, will then become a center for green hydrogen. This can be fed into the existing natural gas grid that extends from the northeast of Germany to the southwest near Stuttgart.

In total, more than 40 companies from the entire H2 value chain presented their solutions and products in the high glass hall next to the conference hall in the Estrel Congress Center. The organizational framework of the H2 Forum was right: There was time to connect during the coffee breaks, lunch and supper. Lively discussions took place at all the tables and stands. That more politicians were present this time than at previous events was, according to Laura Pawlik, Sales Manager of the organizer IPM, particularly emphasized in the feedback from the participants. And also that the representatives from politics and administration were definitely open to further funding.

The date for the next conference has already been set: March 4 and 5, 2025, again in the ECC in Berlin. Focal points will be in addition to politics also the regulatory progress in Germany and Europe.

by Sven Jösting | Apr 15, 2024 | Energy storage, Fuel cells, international, News, Stock market, worldwide

The share of Cummins Engine brings joy: The share price rose to a new high for the year, after the company was able to settle a long-standing legal dispute – it was about non-compliance with emission standards for engines – with a penalty payment of 1.6 billion USD, and with that this chapter is closed. The total cost of this settlement was 2.04 billion USD. Regarding the value per share, Cummins earned a good 19 USD in year 2023, if including the abovementioned costs. So it was about 6 USD per share.

The dividend remains at a high level – recently 1.68 USD per share in the quarter. Turnover increased by ten percent to 34.1 billion USD in year 2023 and should also further grow in the future. The subsidiary Accelera, which concentrates on the clean energy business (engines, batteries, fuel cells, electrolysis, etc.), was able to increase turnover to 354 million USD and should in the current fiscal year bump this up to 450 to 500 million USD. This area belongs, via the program Destination Zero, to one of the company’s future fields of focus and requires considerable investment. This division will therefore report a loss this year of 400 million USD, which, however, has its logical basis in the high initial investments. Even so, Accelera alone was already able to build up an order volume for electrolyzers of 500 million USD. The spin-off of the subsidiary Atmus Filtration Technologies to the shareholders (swap offer) is also about to be finalized. Cummins holds over 80 percent in this. The company will be valuated with 1.9 billion USD.

Advertisements

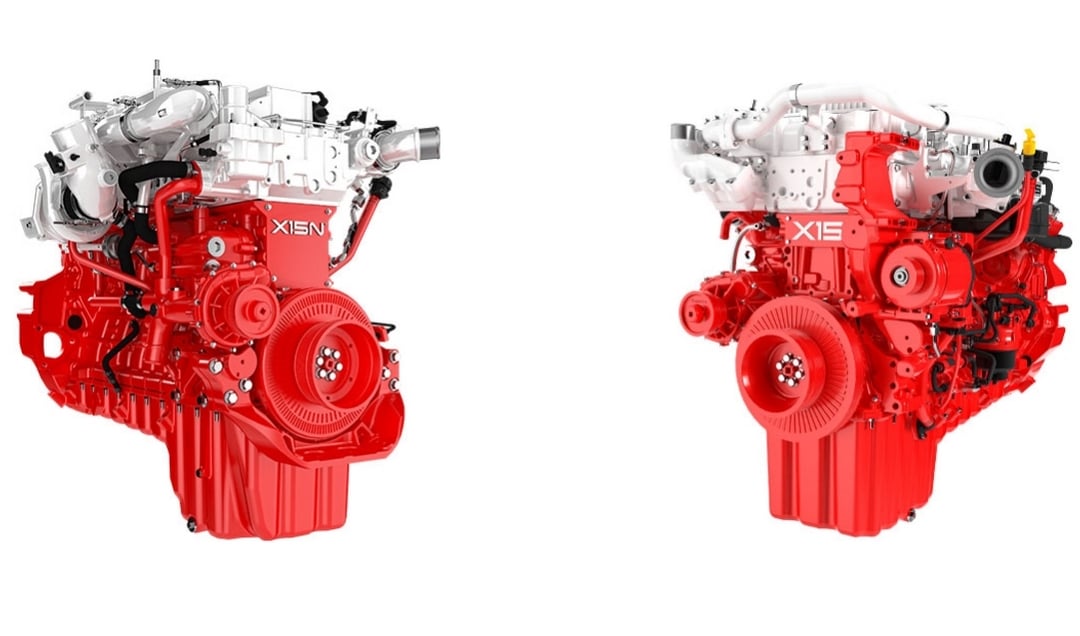

New engine development HELMTM

A share price driver, however, can be the development of a new generation of engines. These units, based on the X15 engine platform, can be operated with natural gas as well as with hydrogen (starting 2028) and e-fuels. HELMTM stands for high efficiency, low emission, multiple fuels. They should accordingly contribute to significantly reducing the diesel demand of today’s customers. Test runs are underway with Walmart and UPS, and also with Paccar for its US class 8 truck Kenworth T680. Cummins is investing 1 billion USD in this project for the time being.

At the current price level – the company has a market capitalization of about 39 billion USD – the current valuation seems sufficient to me, where Cummins is considered a standard stock with a high dividend yield. I would now remember and rather bet on the comparable competitor from China, Weichai Power, as this company is only half as highly valued as Cummins and additionally owns a special potential in the area of hydrogen and fuel cells. Cummins but will go its own way in hydrogen. The subsidiary responsible for this, Accelera, has very high growth potential, which will have a positive impact on the company as a whole in a few years’ time.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Sven Jösting, written March 15th, 2024

by Sven Jösting | Apr 15, 2024 | Europe, hydrogen development, Stock market, worldwide

Sven Jösting’s stock analysis

#Shares from the crypto universe and from many technology companies are currently reaching new highs. Armaments are also booming on the stock market in view of the many global, some war-like, political conflicts. Only the topic of hydrogen and fuel cells is still leading a shadowy existence, with prices at crash level, which however – still – fully obscures the prospects of sustainably produced energy, and above all of hydrogen.

The stock exchange also always works according to the principle of group rotation, according to which always exactly these topics slide back into the focus and center of investor interest that have been completely neglected up to now but have excellent prospects. Precisely why I expect that, after almost three years of falling share prices, the trend will now gradually reverse and a sustainable, long-term upward trend on the stock market is beginning that is based on very high company growth.

Advertisements

To many market participants, it is unclear at this time how hydrogen will be available in large quantities, although it is already clear today that production volumes will increase enormously and prices will fall. All this, however, doesn’t happen overnight: Gigantic capacities in electrolyzer technology – PEM, AFC, AEM, SOFC – must arise to be able to produce sufficient hydrogen.

Hydrogen economy is on its way and will come!

“The H2 economy is on its way and will come,” was the conclusion of the H2-Forum in Berlin (Feb. 19 and 20, 2024, see p. 20). One speaker explained that we’ve now come, after overinflated expectations, “out of the valley of the dead” and on solid ground. Now, it’s all about assessing risks and partaking in concrete projects, which would mean investments in the whole area of hydrogen. From talk to action.

If we take a visionary look into the years 2030, 2035 and 2040, it’s clear what technologically needs to be on course today. Green and, temporarily, blue hydrogen (produced by natural gas reforming – 70 percent less CO2) will dominate and replace gray hydrogen from natural gas, eventually CO2-freely. Regeneratively produced hydrogen will be a raw material that receives a market price as a commodity on the stock exchange. Those producers who have large quantities of low-cost renewable energy (solar, wind and hydropower) at their disposal and have the necessary access to water (above all seawater) will get a tradable commodity that they can sell on the world market, with high profit margins, or use themselves.

In the last case, it can be observed that countries with ideal framework conditions are increasingly thinking about using the hydrogen produced locally themselves, by setting up corresponding industries, instead of selling it to countries like Germany, as energy is a very important location factor.

Hydrogen and the stock market

In countries such as China and individual regions like the US state of California are developing hydrogen strategies that have model character and can serve as a blueprint for the world. In China, over 1,200 H2 refueling stations are to be in operation by 2025. Currently, it’s about 400. South Korea wants long-term to establish more than 1,600 H2 refueling stations in the country. Here in Germany are, as before, around 100 in operation.

Companies with capacities for fuel cell stacks and modules for commercial vehicles are in the starting blocks (Bosch, Cummins, Ballard, Hyzon, Toyota, Hyundai, etc.), because these markets will be huge. Several million trucks and buses can be assumed to be converted to battery or fuel cell (also in combination) in the next ten to twenty years. Hydrogen engines are also attracting a lot of attention, as various prototypes have already been developed (Bosch, Cummins, Toyota).

The question of the right H2 shares can be answered well with this context, as primarily companies will win that have a mature technology, operate with robust business models, are able to deliver and possibly profit from the consumable hydrogen itself, if they can produce it themselves at low cost or distribute and use it as a commodity.

Here beckons the prospect of a good profit margin with high growth potential. On the stock exchange, however, there is right now in the area of hydrogen a phase of disappointment, as firstly everything is not going so quickly and secondly setbacks must also be overcome. In addition to questions of implementation speed, there are often also regulatory issues on the timeline. That the stock market has not yet recognized the potential of the companies through their share prices and valuations is easy to see from the current prices. There is no question that there will be a complete reassessment, however, even if it will take longer. Be patient. We are only at the beginning of this new mega-trend – also on the stock exchange. Let’s wait for the group rotation; then, everything will happen very quickly.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Sven Jösting, written March 15th, 2024

by Hydrogeit | Mar 7, 2024 | Europe, Germany, international, News, Policy

Interview with Jorgo Chatzimarkakis, CEO of Hydrogen Europe

There is a lot that needs sorting out at a political level: A large number of industry representatives are waiting for politicians in Brussels and Berlin to put regulatory safety nets in place so they can make appropriate decisions about their investments. H2-international asked Jorgo Chatzimarkakis, Europe’s “Mister Hydrogen” and CEO of Hydrogen Europe, about the European Union’s revised Renewable Energy Directive (RED III) and its Important Projects of Common European Interest (IPCEIs). The interview also touched on Germany’s 37th Ordinance on the Implementation of the Federal Immission Control Act (37th BImSchV) as well as the recently revealed problems with fuel cell buses and their refueling stations. His guest article about H2Global appears on page 48.

Advertisements

H2-international: Mr. Chatzimarkakis, fortunately the adoption of RED III didn’t take as long as RED II. What do you think of the outcome?

Chatzimarkakis: The adoption of RED III is a positive step for the hydrogen industry in Europe. It provides clarity and the basis for funding and developing hydrogen projects and applications. That said, it’s important that it’s swiftly implemented so that the sector has the necessary planning certainty to make investment decisions.

The extremely arduous procedure for IPCEI projects has been a massive headache for the H2 industry. Apparently there should now be some movement. Can you confirm that and shed some light on it?

Yes, the delays in IPCEI projects have troubled the industry, caused by bureaucracy at either a European or national level. The consequence has been that funding recipients have to wait too long and then they back out. That harbors the risk that projects could be carried out in the USA, for example. We can’t afford to lose any time as the creeping deindustrialization process is accelerated by such unnecessary delays. To counteract this, I was able to get things moving for one process or another. The IPCEI initiatives are crucial for the development of the hydrogen economy and the funding of innovation. It’s important that the bureaucratic hurdles are surmounted so these projects can move forward.

What feedback do you get from your members? Do they regret having applied in the first place?

Some of our members have expressed concerns about the long delays for IPCEI projects. They have invested considerable resources in the applications and are waiting for the green light in order to move their projects forward. It’s understandable that they are frustrated by the continuing uncertainties.

What’s your advice? To forgo funding and start something quickly themselves or to continue to wait?

The decision whether to forgo funding and start independently or to wait depends on each company’s individual circumstances. However, it’s important that funding is released as quickly as possible to support urgently needed hydrogen projects and accelerate rollout.

Sadly, the production of green hydrogen is still associated with high capital expenditure and financial risks. Despite funding, the long-term operation of a plant for producing green hydrogen on an industrial scale is often not viable. That’s why we still need alternative hydrogen production pathways which can produce more competitively.

Let’s turn our attention to Germany: Many have been waiting a number of years for the 37th BImSchV. To your knowledge, when will there be a new ordinance and what, to your knowledge, will it contain?

It’s regrettable that the revision of the 37th BImSchV is taking so long. Unfortunately, I don’t have any precise information on when a new ordinance is expected or what it will contain exactly. However, it’s essential that the ordinance takes into consideration the needs of the hydrogen industry and the requirements for reliable and efficient hydrogen production.

Allow me to ask two or three questions about the open letter that Hydrogen Europe recently received (H2-international has a copy). In it, various high-ranking industry representatives from the JIVE, JIVE 2 and MEHRLIN project consortium ask for an “improvement to the hydrogen refueling infrastructure for FC buses.” Did you receive this letter?

Yes, we received the open letter. We take the concerns of the industry representatives very seriously. Improving the hydrogen refueling infrastructure for fuel cell buses is of critical importance to support the spread of eco-friendly means of transportation. Waste-to-hydrogen, in particular, could be a piece in the puzzle. That’s because the costs of production, for example from biogas, are two to three euros per kilogram. Combined with the GHG quota, that quickly becomes viable.

The letter also says: “The members of the consortium are convinced that FC buses can be a practicable option for public transport throughout Europe. They have proven themselves to be reliable and have been well received by both passengers and bus drivers. However, the consortium is of the opinion that the technical readiness and the capabilities of hydrogen refueling stations (HRS) fall well below the requirements for the operation of an FC bus fleet. The consortium believes that this represents a huge obstacle and a limitation for the commercialization and proliferation of FC buses and could in fact represent a challenge for FC vehicles across Europe and perhaps, indeed, the world.” You are urged in this letter to recognize the significance of this problem and to conduct talks with industry about possible solutions as a matter of urgency. What’s your response to this?

The consortium’s concerns are justified. We’re supporting efforts to improve the hydrogen refueling infrastructure for fuel cell buses. For instance, we and our member companies are actively involved in standardization in this area – for example with ISO and UNECE. It’s important that industry and political decision-makers work together to find solutions to this challenge and to ensure that fuel cell buses are able to realize their full potential.

What’s more, AFIR [Alternative Fuel Infrastructure Regulation] is sure to have a very positive effect on the ramp-up in refueling. It obliges EU member states to build hydrogen refueling stations at central European intersections and in city hubs. We’ve calculated that up to 600 refueling stations in total will need to be built within the EU by 2030. That will give a considerable boost to users of fuel cell buses.

Does that mean you will address this problem – including in the interests of your association members?

Yes, Hydrogen Europe is actively addressing this issue and is advocating for the improvement of hydrogen refueling infrastructure. We are committed to representing the interests of our association members and driving forward the development of the entire hydrogen economy in Europe.

Interviewer: Sven Geitmann

Extracts from the open letter

“If there is something needed for the commercial operation of buses in public transport systems, then it is an HRS that is reliable and available for operation. This basic standard is frequently unmet at current refueling units. Almost all sites in the JIVE, JIVE 2 and MEHRLIN projects experienced considerable downtimes for the refueling unit, meaning that vehicles were not deployable.”

“It took many months to achieve a reliable and robust refueling process, and during that time numerous faults occurred in the course of the refueling process which took considerable time to be remedied by the supplier – and this despite the inherent redundancy of the station.”

“Consortium members report problems with a range of essential hydrogen dispensing equipment. These problems are surprising given the extensive experience of hydrogen handling in industry.”

“Furthermore, the problems and comments are similar to those reported in numerous projects in the early 2000s. It is remarkable and extremely disappointing that the performance of compressors for the refueling of FC buses has clearly not yet reached the level necessary for the operation of a commercial fleet.”

“The project sites have reported that data transmission is often interrupted which causes refueling to stop or leads to refueling taking longer than necessary. The sensor in the nozzle is not robust. If it fails, the entire fuel nozzle unit has to be replaced at a cost of EUR 10,000.”

“Significant problems occurred in buses when tanks were converted from Type 3 to Type 4. At least in some cases, this appears to be due to information from the bus manufacturers not being passed on to the HRS OEMs.”

“Indeed, the HRS availability targets of above 98 percent had already been met, e.g., by some sites in the CHIC project; yet this level of performance was only achieved with considerable deployment of staff and financial input, in other words with higher costs.”

“Commercial operators require their vehicles to be available whenever and wherever they are needed (and at reasonable operating costs). This is perhaps the most important variable considered by operators if they are contemplating investments in new or additional vehicles. If they cannot be certain that the vehicles can be refueled when needed, none of the plans for expanding the fleet of FC buses will go ahead.”

“It is our opinion that the continuing refueling problems must be resolved if the EUR 407 million that have been invested in FC buses over the past 20 years from EU public funds as well as funds from industry, bus operators, SMEs and research partners is to result in the long-term commercialization of the buses. We are convinced that they can be quickly resolved if they receive the necessary attention and the requisite resources.”

by Hydrogeit | Feb 15, 2024 | Germany, News, Policy

Guest article by André Steinau, CEO of GP Joule Hydrogen

After all, the Ampel Coalition leading the German federal government did reach an agreement shortly before the end of the year. And the ramp-up of the hydrogen economy will – again after all – not be completely slowed down, but will continue. But: Among others, the subsidies for erecting refueling and charging infrastructure (“Zuschüsse zur Errichtung von Tank- und Ladeinfrastruktur”) will sink in the climate fund Klima- und Transformationsfonds 2024 by 290 million euros (from 2.21 to 1.92 billion euros), and – the second but – the framework until now was and is for the ramp-up of the hydrogen economy in Germany simply not sufficient.

Advertisements

This is particularly incomprehensible in view of the enormous relevance that hydrogen production has for achieving the expansion targets for renewable energies and thus also for achieving the climate targets. The generation of electricity from wind and sun is in any case dependent on the weather. Accordingly, everything that helps to integrate renewables into our overall energy system, temporarily store their energy and transport it to consumers must be promoted. Electrolysis has a particularly high value here, as it makes the energy in the form of hydrogen usable independently of time and then enables the distribution of the energy through transport on the road, by rail or in pipelines.

A gigantic market is growing here. Sustainable and at the same time vital if we want to avert the worst consequences of the climate catastrophe. In the USA, this has been recognized. There, in the framework of the Inflation Reduction Act (IRA), many billions will be invested in the development of the green hydrogen economy and thus also in the transformation of the industrial sector.

And here? Here, subsidies are still too often viewed as if they were gifts for risk-free entrepreneurship. The opposite is true. For the hydrogen projects alone that GP Joule is just implementing, a good 30 million euros in funding applied for or approved spurred nearly 60 million euros in private investments.

But uncertainty scares off investors, whether banks, entrepreneurs or other financiers. Financing green hydrogen projects is becoming increasingly difficult. Banks are demanding higher risk premiums. At the same time, subsidies are falling – see above – rather than attracting. The German government behaves hesitantly. Previously announced funding programs are a long time coming. All not good signals.

The promised calls of funding for electrolyzers, hydrogen refueling stations and, above all, fuel cell trucks should swiftly be put on the road, because the ramp-up of hydrogen production requires security of purchase. Hydrogen producers, infrastructure operators and truck manufacturers only have this security if vehicles are subsidized.

However, with a coherent policy, the state would need to be not only a giver of consumption security but also investment security as a guarantor. If the financing of hydrogen projects – also due to the international crises from Ukraine to the Middle East – becomes increasingly impossible, it will also become increasingly difficult to produce green hydrogen competitively and cheaply. Banks and companies from the world of capital and finance are indeed looking for ways to finance H2 projects. However, in the current market ramp-up phase, the state is also urgently required to provide financial impetus through industrial and economic policy.

There are plenty of suggestions as to what these impulses could look like, how the state can become a guarantor: instead of pure investment funding, a type of fixed remuneration on the basis of the capacity of the hydrogen refueling station that is payed out over a period of eight to ten years under the condition of a consistently high performance of the refueling station, which makes the now needed infrastructure establishment commercially possible.

The state could also really be a guarantor and provide cheap credits for hydrogen projects, for example through a loan program of the public fund KfW.

For the ramp-up of the hydrogen economy in Germany, strong incentives are urgently needed. The instruments are on the table. If they are not used, Germany could, after the relocation of the solar and wind turbine industries, be facing the collapse of the next crucial pillar of the energy transition. It would not only be bad news for the climate, but also for the country’s economic status.

Author: André Steinau, GP Joule Hydrogen, a.steinau@gp-joule.de