The numbers for the third quarter and the outlook promise a very exciting future for Hyzon Motors and its 200‑kW FC modules for trucks. Series production will begin in the second half of 2024. The activities will be concentrated at one location in the USA. Hyzon with its subsidiary is withdrawing from Europe. That is the right step, since a young company should concentrate on the market that is most important to the company, in order to use the limited capital resources in a targeted way.

Hyzon, however, is still looking for a fulfillment partner in Europe who can independently bring to use the company’s FC stacks, comparable to the partnership with Fontaine Modification in the USA or one like Quantron with Ballard Power. Hyzon is focusing on the USA and Australia/New Zealand, where a hydrogen-powered waste collection truck was recently delivered to Remondis. The FC modules are produced in the USA, which makes sense given the subsidies.

Advertisements

Hyzon will also benefit from the development of the H2 hubs, because the MACH2 project in the Midwest lies in the vicinity of its own production facility and belong to the projects of the DOE subsidized as part of the seven billion-dollar hydrogen hub program (awards of one billion dollars for each hub).

At the same time, Hyzon announced that they have agreed with the SEC to a payment of 25 million USD, payable in three installments over the next few years. This concludes this unspeakable issue, which is based on the misconduct of the former board of directors (accounting scandal). The cash burn per month can be massively reduced, and for ramp-up of module production only about five million USD is required. At the end of the third quarter are still 137.8 million USD in the bank, at a capital requirement of 10 million USD per month.

With the parent company and majority shareholder Horizon from Singapore, the IP license agreement was able to be extended until 2030 and could also be extended to other activities: So Hyzon is also planning to introduce new 300‑kW FC single stacks into the stationary energy supply of data centers and hospitals. Ballard Power and Bloom Energy are already active in this area.

Parker Meeks, CEO of Hyzon, responded to a question about why his company was focusing exclusively on fuel cells and not electric vehicles: „The experience with battery-electric trucks for many has been one in which the usable range is not what they imagined, especially when going uphill, which is the case even in the Los Angeles Basin. If you know the area, if you’re going somewhere where there’s a long distance, you’ll probably have to drive up a hill. Fuel cell trucks do not lose power, and this is the crucial factor that makes them particularly suitable for heavy transport as opposed to transporting drinks.”

Summary: In the USA Hyzon is working on establishing and expanding capacities in order to ramp up production of the 200‑kW FC modules. The partnership with Fontaine Modification suggests that a large sales market is emerging here, as Fontaine rebuilds trucks or retrofits vehicles and Hyzon as a technology partner in this comes perfectly into use with its FC modules. In this context, we can also well imagine that Fontaine through parent company Marmon Holdings has a direct stake in Hyzon. There will surely be capital measures (new issue of shares), and the entry of a strategic partner would be the ideal way to achieve this.

A highly speculative, very interesting investment. Hyzon is suitable as an admixture to Ballard Power and Nikola Motors, as these three companies can be jointly assigned to the area of fuel cells in commercial vehicles.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

The portfolio managed by the author with name BZVision (exchange-traded fund, BZ stands for the German term for fuel cell) on Wikifolio (www.wikifolio.com) perfectly reflects the development of fuel cell shares. After growth of over 100 percent per year in the years 2018 to 2020, the portfolio is now back to square one. While earlier, positions in FuelCell Energy, Plug Power and Hydrogenics (taken over by Cummins Engine) were contained, there are only three securities in the portfolio today: Ballard Power, Bloom Energy and Nikola Motors. Compared to a broadly diversified hydrogen ETF, this is highly speculative. The reasoning for this is that these three titles cover all aspects of the application of fuel cells and hydrogen. Whether transport (commercial vehicles such as trucks and buses, ship and rail transport), energy generation or in-house production of hydrogen. Geography too is taken into account (USA, Europe and Asia). This is not a recommendation. Once a month is a commentary on the portfolio and performance. BZVision: ISIN – DE000LS9QJG9 / WKN: WF00BZH2VI.

Why no recommendations for other FC securities?

I take a very close look at companies such as Nel Asa, ITM, PowerCell, Nucera and many others. As I assume that competition, especially from China, will increase significantly in the field of electrolyzers, it may even be that high growth in orders does not necessarily lead to higher profit margins. Leading Chinese solar cell manufacturers such as Longi are building large capacities in electrolyzers. The quality of these products are not – as talks with experts on site suggest – to be inferior to European producers, for example. However, there are large price differences. At the same time, demand for all types of electrolyzers (SOEC, PEM, alkaline) is increasing dramatically worldwide. Companies like Bloom Energy, Plug Power, FuelCell Energy and Siemens Energy adequately cover the area of electrolyzers as part of their business models – sometimes with technology leadership like at Bloom. Furthermore, the comparison of the stock market valuation of the companies in relation to sales, incoming orders and liquidity is a criterion. Clear, however, is: From the ramp-up of the hydrogen economy, all companies involved will benefit – including in their share price performance. Exciting are the prospects of big gas producers such as Linde, Air Products and Air Liquide. These will especially benefit from the subsidy programs for green hydrogen. In the next issue of H2-international, there will be more background on this.

Advertisements

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

My number one in this segment was and remains Bloom Energy, even if the share price, despite the recent price gains, does not come close to reflecting the prospects. In the third quarter, the turnover was able to rise nearly 37 percent to over 400 million USD. There is much to suggest that the current fourth quarter will also show a strong upward trend – 1.4 to 1.5 billion USD should be the total for 2023. The non-GAAP profit margin was able to rise in the quarter an impressive 12.4 percent from the previous year to 31.6 percent. Non-GAAP profit in the third quarter amounted to 51.8 million USD, so an improvement of 80.3 million USD compared to a non-GAAP loss of 28.5 million USD in Q3 2022. I am concentrating here on the non-GAAP figures, as these exclude special factors and one-off effects.

In year 2024, Bloom should not only be cash flow positive, but also operationally profitable. The cash on hand of 650 million USD at the end of the third quarter must also be seen from the aspect that material inventories with value of over 400 million USD (capital employed) were significantly increased, so existing orders can be processed quickly and, because of the parts on hand, there are no supply chain problems.

Advertisements

Production sites centrally consolidated

Bloom is concentrating fully and completely on the Fremont location, because production there is highly efficiently automated (state-of-the-art facility). As a result, nearly 100 employees were let go (overhead in Sunnyvale), which was interpreted to mean that the company was not doing well (comments in chat rooms and analyses) – by no means the correct interpretation, because higher automation saves on costs. Everything has an upside and a downside.

Exciting is the outlook of CEO K. R. Sridhar: The enormously increasing energy demand – for example for AI – will be drive the business of Bloom and its energy servers, because it’s not just about the quantity of clean energy, but also about its permanent availability (24/7) and security. Power-to-heat models enable the simultaneous use of generated energy for electricity and heat, as the energy generated in the process and its waste heat can be used immediately for heating (process heat) and also for cooling. The perfect cycle. As the electricity grids are reaching the limits of their capacity, island solutions like that of Bloom are coming in the focus of many businesses. While natural gas is still being used for the time being, it will successively be replaced by hydrogen in its many colors.

In parallel, the company’s own carbon capture technology will reduce the CO2 footprint. Here Sridhar also makes interesting allusions to the potential of its own high-temperature SOEC electrolysis. All the same, Bloom with its electrolysis technology is participating in four out of the seven hydrogen hub projects of the Biden administration (seven billion USD investment in seven H2 production centers spread across the USA). The business with the electrolysis will start in 2024, but will then make a real contribution to the company’s growth starting 2025. CEO Sridhar has said, “Bloom Energy is executing at a high level on innovation and growth.” Summary: The stock market story is round. In year 2024, we should see again prices over 30 USD, if the company’s forecasts are met.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Written by Sven Jösting, December 15th, 2023

The Swiss energy corporation Axpo has identified hydrogen as a field for strategic growth. The H2 production facility at Kraftwerk Reichenau – the power plant on Reichenau Island – is one of several set by run-of-the-river hydropower plants that Axpo has planned for the coming years. Because Switzerland is striving for climate neutrality by 2050. Green hydrogen is playing a central role in this – particularly to decarbonize the heavy transport sector.

Advertisements

Axpo is the largest producer of green electricity in Switzerland. By 2030, the energy corporation wants to have installed in the domestic market alone 3 GW of wind power plants and 10 GW of solar. The energy supplier, however, also wants a part in shaping the future of green hydrogen in Switzerland and Europe. Because the Alpine republic currently has a total H2 consumption of 430 GWh, or 130,000 tonnes. In perspective: This corresponds to 0.2 percent of EU demand. And 85 percent of this consumption is alone attributable to the Swiss petroleum refinery Raffinerie Cressier.

First H2 production end of 2023 in Graubünden

Visible results can already be seen from the new strategic field. Axpo and Rhiienergie have installed at hydropower plant Wasserkraftwerk Reichenau in Domat/Ems an H2 production plant with a capacity of 2.5 MW. The plant is to go into operation at the end of 2023. The two companies have together invested the equivalent of over 8.35 million euros. The production facility will be directly connected to Wasserkraftwerk Reichenau, in which Axpo holds a majority interest, situated in the canton Graubünden.

At this site, up to 350 metric tons of green hydrogen are to be produced annually using hydropower. This is analogous to about 1.3 million liters of diesel. The green hydrogen will be delivered from the production plant directly to refueling stations. Alternatively, the green hydrogen could additionally help make energy supply for industrial operations more eco-friendly.

So far, likewise to Germany, hydrogen has not been widely used as a fuel in Switzerland. A network of fueling stations is only slowly being established, although the first H2 trucks are already on the roads. H2 mobility remains a niche area for now. Nevertheless, the current 53,000 heavy vehicles in Switzerland offer great potential for the growth of a future hydrogen market in the coming years. A demand of around 5 t H2 per truck per year from this market is quite realistic. If so, 30 percent of the vehicles would then require 80,000 t H2. At 5,000 operating hours per year, this would necessitate an electrolysis capacity of 1,000 MW.

Environmental and heritage protection prevent expansion

Not all of the innovative projects will see a successful implementation, as the resistance from some persons with an interest in nature and heritage protection is in some places simply too strong. One example is wind energy: The time for the planning and design phase of projects is enormously long; time and again, they do not advance. The result: In the whole of Switzerland, just 41 wind power plants are running. Axpo operates only one of these, through its subsidiary CKW.

But the protest is not limited to wind power alone: Earlier this year, an H2 project on the Swiss-German border was halted due to objections made by local residents (see H2-international Feb. 2023). “The hydrogen production facility at Wasserkraftwerk Eglisau-Glattfelden has been tanked as a result,” confirmed Axpo CEO Christoph Brand. Three private individuals had lodged protests. They did not want one truck once per day driving through their residential neighborhood and picking up the hydrogen, Brand explained. In addition, however, a power generation structure erected outside of the developable land zone will have to be demolished and placed elsewhere, as the court did not grant it exception approval from the zoning. The H2 plant when finished was to likewise have a capacity of 2.5 MW and produce around 350 tonnes of green hydrogen annually. That is now history. The green gas must come from elsewhere – from Northern Europe, among other places.

Fig. 2: The H2 plant under construction

Luka Cuderman, who as energy manager at Axpo is working on the strategic direction of the future H2 business, summarized the general requirements for an H2 production site once more. So the power plant itself needs sufficient space and connection capacity. Outside of the buildable land zone, according to his statements, certain constraints must furthermore be met in order to conform to zoning restrictions and be allowed there. Equally important are proximity to end consumers as well as a good connection to transport routes. “A secondary application such as utilization of incidental waste heat is a further plus,” stressed Cuderman.

The electricity price is the determining factor for H2 costs here. It accounts for more than half of the total cost. The investment costs, the capex, of the plant are in turn directly linked to the number of operating hours. An increase of this working time is only sensible under certain conditions, however, since operation at high electricity costs is uneconomical. “For the example of an electrolyzer with 2.5 MW, we assume 5,500 operating hours,” stated Cuderman. The cost of operating the plant, or opex, accordingly accounts for twelve percent of the H2 cost per kilogram. Grid costs do not incur for the operation if the H2 plant is directly connected to the power source. That is, however, not always the case.

Summary: The more hours an electrolyzer can work, the more weight the electricity costs take on. So close to full load, the cost for electricity constitutes 80 percent of costs.

2,000 t H2 per year from Aargau

Axpo wants to advance the topic of hydrogen in its homeland in another way: At the industrial park Wildischachen in the canton Aargau in Northern Switzerland, a still larger production facility is to soon appear. It is designed to have up to 15 MW of installed capacity. Annually, 2,000 t of hydrogen is to be made available. The electricity required for production is coming entirely from the nearby run-of-the-river power plant Flusskraftwerk Wildegg-Brugg. With direct connection to the hydropower plant owned by Axpo, climate-neutral production of hydrogen will be ensured.

The H2 produced will then be delivered partly to the nearby refueling station of company Voegtlin-Meyer via a pipeline and partly to other refueling stations in the region. The green hydrogen is to be made available to private users, on the one hand, as well as used in H2 buses for public transport commissioned by the company PostAuto. With the produced H2 quantities, around 300 trucks, PostAuto vehicles or buses can be run per year.

The utilities provider IBB is designing the pipeline that will lead from the H2 production plant to the refueling station in Wildischachen. The waste heat resulting from the electrolysis process is to be utilized in the heat network of neighboring industrial operations. The location of the plant is therefore ideally selected, as it is in the direct vicinity of the Axpo hydropower plant in Wildegg-Brugg and of the refueling station of Voegtlin-Meyer. The construction and start-up of the H2 plant is planned to occur in the course of 2024. Which is when the fleet of PostAuto is to be supplied with green hydrogen. So in Switzerland as well, the niche for green fuel is starting to grow.

In recent years, hydrogen has managed to move out of its niche and onto the political main stage. Not just in Germany and Europe but across the world, the energy sector is bracing itself for change as we move from the fossil fuel age to a renewable era.

Advertisements

While some regions are only slowly preparing themselves for the real energy transition, many countries in central Europe as well as nations like the United States and Japan are right in the thick of it. The introduction of the Inflation Reduction Act saw the US roll out a huge financial package. Such a step has yet to be taken in China. The People’s Republic has long been at the forefront of electric transportation but the political framework for instigating a hydrogen economy remains a work in progress (see p. 48).

Germany, on the other hand, was at the cutting edge when it coined the term “energy transition” many years ago, an expression that now, around the globe, epitomizes this transformation process. And by phasing out coal and nuclear power and cutting back on oil and gas, Germany finds itself in a good position, but we are no longer at the forefront when it comes to tackling the climate crisis.

For a long while, Germany was ahead of the field when it came to the environment – leading on solar and wind technology as well as hydrogen and fuel cells. The hope is for a better result this time when establishing its own hydrogen and fuel cell industry than was the case for photovoltaics.

The German government recently adopted the update to its national hydrogen strategy, thus making clear its support for the course it set three years ago (see p. 14). What’s more, Germany is now getting a steering committee for hydrogen standardization so it can launch a standardization road map for hydrogen technologies (see p. 6).

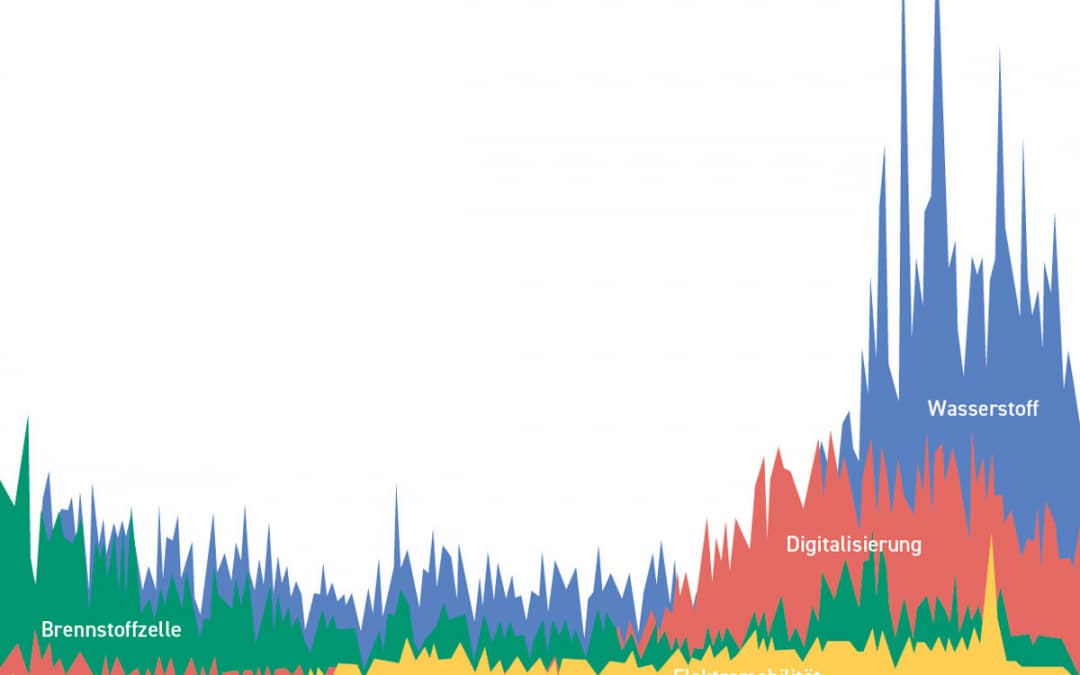

With so much happening, it will come as no surprise that, in the German-speaking world especially, the word for “hydrogen” (Wasserstoff) has for many months been a popular term in online searches. Interest in hydrogen began to grow at the end of 2018 – well before the market started to ramp up, as research using Google Trends clearly shows (see p. 7). At that point, the number of inquiries using the Google search engine increased considerably, exceeding the 2004 level in early 2019.

Since then, the US corporation has recorded ever-higher numbers of searches for this particular keyword. In early and mid-2020 and early 2021, hydrogen inquiries overtook searches for the German equivalent of “photovoltaic” by a wide margin. Over the years, “hydrogen” almost always outperformed German inquiries for “fuel cell,” “electric mobility” and “digitization” (see cover graphic for German search results with keywords translated into English).

Globally the situation is a little different: Throughout the past two decades, a comparatively high number of Google users have looked up the word “hydrogen” in English – far more frequently than the English words “fuel cell,” “photovoltaic” or any spelling of “digitization.” Only “PV” enjoys a similar popularity to “hydrogen.”

Of course, this kind of trend analysis isn’t rigorously scientific, but it does give a representative indication of the interest level in hydrogen now, and how that compares with the past. Our analyst Sven Jösting, who has been monitoring the stock market performance of hydrogen and fuel cell companies for many years (see p. 47), has for a long time talked about a “megatrend.”

To all the critics who say it’s just another hydrogen hype, I can confidently reply: It is extremely likely that this time we’re looking at a proper hydrogen boom. And we’re right at the start of it.

For it’s only early days as we still don’t have a functioning hydrogen market. Except, that is, if we look at hydrogen as an industrial gas for conventional applications (welding, medicine, etc.). Preparations are underway, however, by H2Global to set up a trading platform that will enable hydrogen to be bought and sold in large quantities in a similar way to how the European Energy Exchange operates.

It’s also true that we don’t yet have a market for electrolyzers or fuel cells. Unless, of course, you count the hitherto low production volumes and capacities. This is essentially negligible in view of the quantities and capacities that we will potentially need. Hopefully we’ll be able to report on the latest sales and installation figures in the February 2024 edition of H2-international.

Even in the mobility sector, sales are still extremely modest, which is why no real acceleration of the market can be assumed before 2025. That said, this will only initially affect the commercial vehicle sector, i.e., hydrogen trucks and buses. In all probability, hydrogen automobiles will only be produced and sold in significant quantities at the end of the decade – if that does indeed happen at all. It will take even longer for rail vehicles, ships and airplanes.

The outlook, however, is clear: As the world shifts increasingly away from fossil resources, so renewable energy becomes ever more important. The upshot is that we need a lot more solar power plants and wind turbines. And hydrogen will be essential in bringing this vast quantity of green power to the different energy sectors.

Admittedly, it’s a pretty basic description of the energy transition. Though it does plainly show that hydrogen, far from being just a megatrend, is something that the energy sector simply can’t function without.

That the wind subsidiary Siemens Gamesa will still cost its parent company a lot of money has been the case for a while. Too great are the problems with some wind turbine types (onshore), and integration also costs money until synergies properly take effect and cost reduction potentials can be leveraged. Siemens Energy itself still see financial risks with this in the area of 1.5 to 1.7 billion EUR. It could, at the end of the day, as well be two billion. Provisions amounting to 1.6 billion EUR have already been set aside for this purpose, which will come into use in the coming two years. The second quarter brought an overall loss of 2.9 billion EUR (minus of 4.5 billion EUR for the entire year is expected). That’s as far as the negative news.

The good news: Siemens Energy will well be able to cover these losses (liquidity at over 4 billion EUR), even if this will have a very negative impact on the overall result for the current fiscal year and it could take one to two years to return to positive figures. Look at the bigger picture: The order intake worth tens of billions is reason to celebrate. In addition, the risk has now been named, so the stock market will be able to include this in its investment decisions. Investors with time to allow should profit from the turnaround through again rising share prices.

Advertisements

The stock market adage “buy on bad news” is the perfect as a basis for the invest in Siemens Energy. Because Siemens Energy with an order volume of over 110 billion EUR is virtually flooded with orders relating to energy security, hydrogen and the like, but there are not many companies in the world that as a one-stop shopping partner are able to offer everything from a single source. Many of the business units are doing very well and are highly profitable.

If the share price weakens further, 13 or even 12 EUR would be the perfect entry price as well as usable for the price reduction of old stocks. In two years, I expect prices of over 30 EUR.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.