The interest rate hikes in the USA, necessary to combat inflation and already in prospect, is putting stock markets around the world to the test. Such a damper, since this economic development will affect the growth of companies, as consumers will be more inclined to reduce their expenditures. That’s sure to the case in many instances, as rising costs for energy and food are placing a heavy burden on numerous households. In the US, consumers, which account for nonetheless two-thirds of the gross national product, are the basis for the economic growth that is therefore based on demand by them. But the US Inflation Reduction Act promises a lot of good things for the H2 and FC sectors in particular.

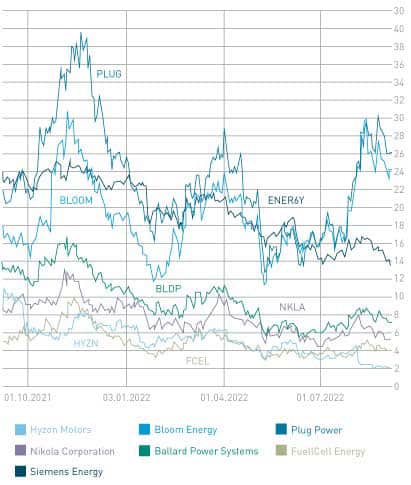

Share price performance of the companies discussed

Advertisements

Source: www.wallstreet-online.de

The Inflation Reduction Act already in force stands for the topics of energy security, decarbonization and electromobility in the USA and of course provides massive support to companies that are active in the field of hydrogen and fuel cells there. And it is specifically these companies that we cover here in this stock analysis, as they – worldwide – are on the verge of tremendous, sustainable corporate growth. Which of course also has a positive effect on the associated share prices.

Advertisements

Thus, there will not only be losers on the stock market, but also winners with technologies and business models that are good for the climate. And that stand for falling energy prices, when hydrogen as an energy carrier becomes available in ever larger quantities at ever lower prices and competes with fossil energy carriers. At the end of the day, this is then even one of the many ways to counter inflation via falling energy prices, which should please Federal Reserve chairman Jerome Powell, even if inflation in the US is, at the moment, still being combated with rising interest rates.

The shares discussed here might even end up among the winners, since stock traders do not orient their actions only according to the general economic situation, but also assess an individual case or an entire industry according to its outlook. Institutional investors, such as BlackRock, even set this as an investment focus.

Investors with a medium-term investment horizon need not be alarmed by this if they hold shares in the hydrogen economy and should maybe even have bought again, bit by bit, since the trend of this market is very predictable – in a positive sense. On top of that, many of these – examples are Ballard Power and Nikola Motors – are at a low price level. Where – despite rising interest rates – medium-term, the share price is more likely to go sharply up than further down, if the companies would only implement what they themselves forecast. But that’s just my personal view of things.

Of course no share can escape a general stock market trend (a bear market due to interest rate expectations), but there are at all times winners and losers. The former will be found on the stock market in the hydrogen sector, because all the arguments are in their favor. And many stocks in the US H2 and FC sectors are trading at crash levels, when looking at the share prices from the turn of the year 2020/21 in comparison. Which are also in total contradiction to the milestones achieved in the meantime.

American climate bill finally passed

The Inflation Reduction Act was the result of a very close vote. In the US Senate, the bill passed with 51 votes to 50 and with ex officio Senate president and US vice president Kamala Harris breaking the tie. On August 12, 2022, the bill passed in the House of Representatives with 220 votes to 207. After its signing by President Joe Biden, the law is now in effect and will lead to the implementation of many a climate-related funding program in the USA. A leg up for companies that are engaged in this topic, and above all for many, if not all, of the companies discussed here.

Drawn-out process

This was initially preceded by a no vote from Joe Manchin. And so he was the only Democratic senator to deny support for the Biden administration’s comprehensive plans regarding climate change and thus blocked important decisions, since a stalemate was created between Republicans and Democrats in the Senate. It was like he was the finger on the scale. But now Manchin has agreed to the program upon certain conditions. In addition to the provisions for measures against climate change, there will also be a debt reduction (minimum tax for companies, closing of certain tax loopholes, price negotiations for medications, and more).

In total is a formidable 369 billion USD, which is to be invested in e-mobility, solar power and wind energy (production facilities/projects for solar panels and wind turbines, R&D) but also to promote energy efficiency measures as well as carbon capture. Hydrogen especially is a topic of importance. Here, the range extends from a tax credit of 0.60 USD per kgH2 (base rate) for the production of green hydrogen up to a 3 USD per kgH2 production tax credit if the facility for green hydrogen meets additional criteria. The aim is to promptly make green hydrogen competitive with hydrogen obtained from natural gas.

Additionally, the act includes funds for research and development of, among other things, electrolysis technologies to make the production of hydrogen more efficient. Forecasts see the H2 price at 1 to 2 USD per kgH2 by year 2030. Instead of claiming tax incentives (tax credits), there is also the possibility for companies to opt directly for payments (grants). Which is good for their liquidity.

On the topic of decarbonization, there will be tax incentives for carbon capture measures (storage/deep well injection = CCS). Here, 85 USD per tonne of CO2 will be granted. If CO2 is stored in the earth under gas or oil fields or even experiences another use in industry, it’s 60 USD per tonne of CO2.

The whole program therefore covers perfectly a variety of different areas for decarbonization in the US and that address climate change through technology and market-based approaches. Comparing the program with similar ones in Europe, the US is really stepping on the gas, while Europe unfortunately still seems rather reserved with its programs. Even the 1 to 2 billion EUR set aside in Germany for subsidized purchase of hydrogen from around the world via the project H2-Global pale in comparison to the plans of the US. For the US companies discussed here, like Bloom Energy and Plug Power, the planned new programs are to be seen as a turbocharge for the individual business fields and will have a very positive impact on their share price performances – maybe not tomorrow, but in the future will there be positive effects.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

The figures for the second quarter should be published August 15, 2022 at the latest, but Hyzon surprisingly reported that certain sales in China were not followed through in time to be able to be booked (“revenue recognition in China”) and that there are “operational inefficiencies” at Hyzon Motors Europe B.V., the subsidiary in Holland. Earlier statements (balance sheet publications) are therefore invalid or obsolete for the time being. This is a real shock after all the news about orders, corporate partnerships, production ramp-up and the recent acquisition in Germany.

Craig Knight has left Hyzon

Advertisements

Hyzon has time from now to October 14, 2022 to file the necessary figures for the second quarter as well as the corrections for the previous quarters with the SEC (US Securities and Exchange Commission) and Nasdaq. After that, there is an optional extension of 180 days if the deadline cannot be met.

“The Company’s Board of Directors (the “Board”) appointed a committee of independent board members to investigate, with the assistance of independent outside counsel and other advisors, certain issues that were brought to the attention of the Board by Company management. These issues include revenue recognition timing, presentation, internal controls and procedures, primarily pertaining to its China operations.”

Advertisements

Hyzon

That the board chairman, Craig Knight, is immediately leaving the company, having been relieved from his post, suggests that something major must have gone wrong. The new chairman will be Parker Meeks, who was previously chief strategy officer – a McKinsey man with an impressive career. He will temporarily lead the company as interim CEO until a suitable new CEO is found.

Acquisition of the ORTEN Group

The expansion of the company is proceeding according to plan despite the aforementioned problems, as the production facility in Rochester, NY and Chicago, IL demonstrate, as well as the start of MEA (membrane electrode assembly) production in the US and the current job ads for new personnel suggest. Hyzon has additionally received a funding decision and can now apply for state subsidies for trucks in the US (California and New York).

In order to better position itself in Europe, Hyzon has acquired the ORTEN Group (ORTEN Betriebs-GmbH and ORTEN Electric Trucks GmbH), one of the pioneers in the conversion of used and new diesel to battery-electric and hydrogen-powered trucks. With this, 80 employees have moved over to Hyzon, and it is also a good complement to the activities in Holland. Hyzon Europe ORTEN makes mainly trailers and truck conversions for the beverage industry of up to 26 tonnes load weight. Hyzon is thus also entering the battery-electric sector, like Nikola Motors has already. The aim is to be able to offer the shipper or truck buyer several options. The retrofitting of existing vehicles (chassis of diesel trucks) seems an important optional step. Thus Hyzon is addressing the right market and wants to be active not only in Asia but also in Germany and Europe.

DB Schenker intends to rent out Hyzon trucks via hylane

Cooperation with Schlumberger

Major corporation Schlumberger is known mainly for oil drilling, where it is one of the heavyweights. Now the two have started a joint development program in which Hyzon’s FC stacks are to be put into use in various heavy devices and vehicles as well as oil drilling platforms (rigs) for Schlumberger. These can be energy systems on drilling platforms as well as other heavy-duty equipment. The goal is to operate a drilling platform completely with hydrogen energy-wise (2.5 tonnes per day).

In the fourth quarter of this year, there will be a first joint showcase project, according to the press release. Typical 4-MW diesel generators are to be replaced by fuel cell systems. With such partnerships, new emphases are to be set. It’s an accolade for Hyzon to be running a test series with a company like Schlumberger and perhaps then receiving larger orders. I would rather have seen a company like Cummins Engine in this position, only theoretically. But for Hyzon, this is a good and important step by which to bring its own FC technology to a wide audience.

In addition, there will be a memorandum of understanding that will be filled with content from a concrete project. In the coming twelve months, the Schlumberger subsidiary Ensign Energy Services Inc. will integrate a Hyzon FC system into an existing oil platform. Side note: Hyzon developed its own fuel cell technology throughout more than 20 years of research and is therefore not dependent on suppliers of such.

It is clear to us that the company, after all matters have been clarified, is executing its corporate strategy as planned, as already indicated by the presence of the interim CEO at specialist conferences. The share will certainly remain very volatile, owing to the existing uncertainty. Should after deduction of all possible losses and after balance sheet adjustments, among other things, the cash on hand still amount to over 300 million USD – it was over 400 million at the end of the first quarter – the stock exchange should take this into account in the valuation of the company.

I would say: Buy on bad news – but only for investors with a very speculative attitude and traders who know how to use daily fluctuations in the share price to their advantage. The course will have to be a bumpy ride – a roller-coaster ride. Perhaps a competitor is also using the situation to get on here and take advantage.

Investment banks like JP Morgan have of course revised their estimates downwards following the latest publications, though do not advocate selling now and completely breaking up with Hyzon. Is a 400 to 500 million USD loss in value at the stock market justified by the current situation of uncertain information? After all, Hyzon has many high-profile investors. In addition, blocks of shares held by insiders account for more than 60 percent of shares issued.

We’re going crazy: On the one hand, the important trust in the company is lost until clarity (figures, financial statements) is achieved. There may be adjustments for certain financial transactions (stock purchase by Holthausen and transformation of Hyzon Motors Europe B.V.?), if therein lies the problem – and only if. What’s clear: Class action lawyers may be able to take advantage of the situation. Rejoicing are the short sellers, who in the meantime had bet about 20 million shares on a price drop. On August 5, 2022 alone, the share price fell by over 38 percent. Now short sellers can profit massively from this, while some others might also think of tucking in until the time the company provides clarity.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Startups in the hydrogen and fuel cell industry, such as Enapter, Lhyfe and Clean Logistics, have received fresh equity via the stock exchange to implement their business plans and to evolve robust company stories from mere visions. The stock exchange is indeed also the right place to spread the investment risk over many shoulders (institutional and small shareholders). Investors willingly provide the necessary capital so that they can push along the company’s growth with their own strength.

At a premiere celebration for Clean Logistics’s fyuriant (see p. 36), André Steinau, managing director of GP Joule Hydrogen, announced to H2-international that its parent company had just reserved 40 assembly stations for 40 fyuriants:“We will solve, with the production of H2, the building of H2 refueling stations and the offering of vehicles, the well-known chicken-and-egg problem.” Shortly afterwards, CL and GPJ signed a framework agreement for the supply of 5,000 H2 trucks.

Advertisements

Further share issuances have a high probability of following, in order that the company can perfectly finance things itself. The company often has, through the IPO and the stock market listing, quite generous company valuations, calculated by the total number of shares multiplied by the stock market price. Here, it must be taken into account that the number of freely available shares – the free float – almost always comes out to be very low and the overall valuation of the company on the stock exchange therefore corresponds instead to a theoretical value, since the vast majority of shares are held by the company’s founders and management.

An investor in these stocks will have to think about how long they plan to hold the investment. Because these companies will initially write losses, as a result of the use of capital obtained via the stock exchange. There must first be a building up of production capacity, which must be done from scratch. In addition, specialist personnel are needed to turn the plans into reality. Is it therefore possibly better to realize quick price gains after the IPO (initial public offering)? Can the companies constantly come up with (good) news, which is a prerequisite for higher, so raising of, share prices?

Advertisements

In a nutshell: The abovementioned shares are better acquired as a package via a fund, since with the spread of risk over many different stocks in the area hydrogen and fuel cells, the overall trend and a whole industry can be better assessed than in the case with individual stocks. In such funds are of course also heavyweights that are blue chips at the stock exchange and, with their lower volatility, provide a balance to the strong price fluctuations of the small stocks.

Examples here are Siemens Energy, Linde, Air Liquide, Weichai and Cummins. Because clear is: Small companies in the startup range with the designation small- or microcap are much more volatile in their price performance than stocks with very high market capitalization. With a fund, this volatility is balanced out or minimized, since investors participate in the overall trend of this strongly growing segment by raising the prices.

Additionally, a sensible strategy may be to not make a one-time investment, but rather to build up an invest over a longer time period, for example monthly tranches. This would make use of the so-called cost-average effect (dollar-cost averaging). You gain a good average price course over time from the fact that the fund is always valued differently, so you receive more or fewer shares for the same monthly investment amount. With a horizon of ten years or longer, you are statistically always right, as this time period will see some bull markets and some bear markets and you can buy again at sometimes high and sometimes low prices along the course and obtain a very good average annual return.

Also to consider: For hydrogen and fuel cells, the megatrend on the stock market is just beginning. This means that such investments have above-average potential to increase in value and can be dubbed “sustainable.”

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Nikola Motors is on the right track. Various test trials of the Tre BEV battery-electric models are running successfully with customers like TTSI, Tiyaji Brothers (for Anheuser-Busch), Univar, Road One (for IKEA) and Covenant (for Walmart). So far, everything with 94 percent manufacturing capacity utilization. In the second quarter, 15 Trev BEVs were produced and 48 delivered. The preliminary quarterly turnover lay at 18.1 million USD.

The loss for the quarter lies at 173 million USD. So a minus of 0.41 USD (GAAP) or 0.25 USD (non-GAAP) per share. Included are the legal fees in association with company founder Trevor Milton in the amount of 13 million USD as well as stock-based compensation in the amount of 54.8 million USD. Also strongly increased freight charges of over 13 million USD were a factor in this. In cash and cash equivalents, Nikola had at the end of the second quarter 529.2 million USD at its disposal and additional equity lines (Tumim/3i) in the amount of 312.5 million USD – which together makes 841.8 million USD.

Advertisements

The acquisition of the battery manufacturer and supplier Romeo Power for 144 million USD in Nikola shares still lay within the existing authorized capital of up to 600 million shares. Issued were so far 433 million shares as well as 62 million option rights (employee shares and bonus programs) and 71 million shares set aside for convertible bonds. All these together are then 567 million shares with previously authorized capital in the amount of 600 million shares. Now, it could potentially become 800 million shares, since 66 percent of shareholders at the last annual general meeting voted in favor of this. The issuance of shares can now take place from time to time and bit by bit ATM (at-the-market), but that won’t come until 2023 or later, and certainly not at these severely depressed stock prices.

Romeo Power creates independence

Advertisements

Romeo Power was acquired in exchange for shares, so purely with Nikola’s own equity. Romeo should have the potential to sink the annual costs for batteries by 350 million USD by 2026. Together with Romeo Power (former top talent from SpaceX and Tesla had founded the company), Nikola plans to go double-track with the batteries. Romeo, with its production site in the US, is to serve this market, while battery supplier Proterra is to be Nikola’s partner for the European market.

The price to purchase Romeo Power, an equivalence of 144 million USD, corresponds to just nine percent of the stock market value achieved in the meantime. On top of that, Nikola is giving a liquidity grant in the low two-digit million-dollar range to Romeo. What does Elon Musk (Tesla) think of this? Isn’t he himself planning to introduce a battery-electric truck?

Establishment of an H2 infrastructure

In the second quarter, six beta copies of the hydrogen-powered Tre FCEV were sent out for testing. Mass production of these will not start until the second half of 2023. Before that, the H2 fueling stations must be in place. An installation, according to information by the company, takes more than a year, because of the approval process.

So far, the company has launched three H2 fueling stations in California, which are to be in operation the fourth quarter of 2023. So perfect timing in solving the chicken-and-egg problem and freeing hydrogen production. Nikola will operate some H2 fueling stations itself, but also many with partners. Partnerships for this with oil and gas companies are still to come in the current second half of the year.

Modern workspace

NIKOLA_TRE_BEV 7.jpg

Source: Nikola

The Biden administration’s climate act is creating US-wide tax incentives that stretch up to 3 USD per kg of hydrogen. In California, there is an additional subsidy of 3 USD on top, so in total 6 USD per kg can be gotten there. Nikola is assuming that it can self-produce hydrogen for 3 USD per kg. That makes for a very high profit margin.

The factory in Coolidge, Arizona is to have a capacity of 20,000 trucks at the end of the first quarter of 2023 – of both types, the battery-electric and the hydrogen-powered. And it is to be 45,000 units altogether in 2024.

Meanwhile, it became known that out of the cooperation with Iveco in Ulm, Baden-Württemberg – a contract manufacturing agreement – is to now come a closer joint venture, with joint engineering and joint production. My take: Something is coalescing there. Is Iveco, or alternatively parent company CNH, increasing the share in Nikola, which has been 6.7 percent for some time now?

Lohscheller joining the presidents

Board chairman Mark Russell – he pulled Nikola out of rough water (holds about 9.6 percent in Nikola, a value of 260 million USD) – remains on the supervisory board, but will leave his post of CEO to Michael Lohscheller on January 1, 2023 (see also H2-international August 2022). Lohscheller had led the refurbishing of Opel, which today is part of Stellantis. Steve Girsky, former board chairman of GM Europe, is becoming chairman of the supervisory board at Nikola.

Food for speculation

Interesting in this context is that it was General Motors (GM), who was interested in a cooperation with Nikola at the time of CEO Trevor Milton, that was spoken ill of. As it goes, they wanted to build a hydrogen-powered SUV together, and GM was to receive a Nikola share package equivalent to the value of the activities (production/contract manufacturing). The deal fell through for a number of reasons, which are to be found in Milton’s personage.

Could perhaps a cooperation offer itself again, though, with solid support from the top managers of Nikola? This already sounds propitious, since Nikola’s strategy, to offer electricity and hydrogen itself as an energy solution (consumable) and to establish a unique infrastructure network for this, is gaining imitators. Getting involved could give it some speed.

What if Tumim/3i, a VC fund, has started or plans to look for another address for the investment in Nikola (maybe GM or CNH/Iveco?), passing the package on with a markup? Even Tesla could be interested in buying Nikola, after all arguments are weighed. While all vehicle manufacturers have their own strategies for commercial vehicles like trucks, they may find joy in strategic investments in infrastructure and alliances.

Nikola formally offers itself for all this, as the listed market value of 2.6 billion USD is far from the earlier, majorly overstated assessments and there is the opinion that the current stock market value now only reflects the battery area. Former GM managers Lohscheller and Girsky will ensure a new reputation for the company. Does Trevor Milton know something more? He very recently bought 3 million more shares at the price of 5.80 USD per share.

Summary

The stock market still needs convincing, as the share price went from under 5 USD to over 8 USD and then back down below 6 USD. Again were a whopping 78 million shares (mid-August) sold short. If something spectacular were to happen, then Nikola could again be valued completely differently and much higher. Overall, everything is on track. Highly speculative with high hopes.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

FuelCell Energy sees itself as a leader in the CCS sector, where it is a frontrunner as a result of having its own carbon capture technology. With ExxonMobil, FCE has been active in such projects for years. Now the new climate protection program by the Biden administration may provide new potentials for orders, since the tax incentives, with amounts of 60 to 85 USD per tonne of CO2, signify for many affected businesses an impetus, but also a pressure, to upgrade here technologically.

True, it would be logical for cooperation partner ExxonMobil to exert some positive pressure here, but follow-up orders have so far failed to materialize – they’re only doing research together. But also clear: There is now another incentive to avoid CO2 emissions, because you could be charged with penalties otherwise. For FuelCell Energy, this is surely a turbocharge for new orders, along with the incentives for the use and storage of emitted CO2.

Advertisements

For now, we’re waiting until there are concrete orders. The Inflation Reduction Act will have a positive effect either way. The company, however, must prove this with orders. Currently, it’s valued at about 2 billion USD. With over 400 million USD in the bank, FCE takes sufficient account of current developments. For comparison, Bloom Energy has an order backlog of over 8.5 billion USD and already makes 1 billion USD turnover. According to statements by the company, FCE plans to generate a turnover of 300 million USD by 2025, and increase this to over 1 billion USD by year 2030, with a simultaneous sharp increase in profit margin.

Disclaimer

Advertisements

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

More is unimaginable, looking at the share price development of the past weeks for Bloom Energy: from 16 USD to over 31 USD, corresponding to a near doubling. The price decline that then occurred was the fault of a type of arbitrage, as Bloom had announced a capital increase at short notice and issued 14.95 million new shares at 26 USD, so traders were able to sell short at over 30 USD and stock up again at 26 USD – a common strategy that explains the recent fall in price.

But the outlook is favorable. The reason is the prospects given by the figures published for the second quarter: Bloom is maintaining a turnover of over 1.1 billion USD for the entire year as well as the targeted growth (30 to 35 percent over the next ten years) and profitability.

Advertisements

The climate plan within the framework of the already passed Inflation Reduction Act is highly instrumental in this. Bloom is benefitting, according to its own calculation, nine ways from the planned subsidy programs of the Biden administration. Specifically:

Tax credit and/or grant for H2 production of 0.60 to 3 USD per kg

Sales potential of the Energy Server strongly rises

Waste-to-energy segment gets a push to promote biogas applications

E-mobility subsidy programs create potential for home/company on-site charging solutions

Micro-grid deployment receives boost from tax incentive programs (energy security)

Carbon capture tax credits make FC power plants more attractive

Tax credit for production facilities in the USA (Manufacturing Tax Credit)

Subsidy program for regenerative energies

Financing programs for many projects of Bloom’s (direct pay and transferability)

Furthermore, news has reached us that a test program with the Idaho National Laboratory of the DOE (Department of Energy) was very successful and has given proof that the high-temperature fuel cells from Bloom yield 30 percent higher performance than PEM and alkaline electrolyzers. The project involved the use of surplus electricity from a nuclear power plant to produce CO2-free hydrogen from this electricity. For this, Bloom also worked with Westinghouse. It can be assumed that results from these test series will be implemented commercially on a large scale. Westinghouse is technologically involved in over 50 percent of all nuclear power plants.

Advertisements

Independent energy supply via Bloom Energy Server

PHOTO – Utility.jpg

Source: Bloom

The increasing demand globally for energy generated CO2-free is giving wings to all aspects of Bloom’s business model. It’s about energy security and issues like sustainability. For the pilot project of a dairy farm of CalBio, Bloom received the U.S. Dairy Sustainability Award. Manure and dung from cows serve as the basis for the production of biogas, which is then used in fuel cells and equally as an energy supply source for battery-electric vehicles – all in one. Follow-up projects can emerge from this pilot worldwide.

Bloom sees itself on its best path to offering alternatives in energy production. Also energy security through FC power plants as micro-grids that are not connected to the public grid belongs to the future that many companies, as well as customers such as hospitals and data centers, are counting on. Bloom offers technological solutions. The electrolysis capacity is to reach 2.5 GW by the end of 2023 – an enormous leap for hydrogen.

Figures for the second quarter

Turnover in the second quarter amounted to 243 million USD, which was within the range of expectation. The non-GAAP loss lay at 118.8 million USD, which included, among other things, a depreciation of over 40 million USD. Per share, a minus of 0.20 USD non-GAAP and of 0.67 USD GAAP. And 1 GW of new annual energy output has been installed with the recent opening of the production facility in Fremont, California. There, 400 new employment positions will be created.

With the introduction of the new generation of Energy Servers, the operating profit margin will move, which currently lies at 20 percent (target: 24 percent non-GAAP gross margin). The turnover for the entire year is to rise to over 1.1 billion USD. Which means that the two quarters of the second half will see very high growth.

Motley Fool about Bloom

The US stock exchange service Motley Fool has named two companies that are expected to have above-average growth, in terms of stock price performance as well. Bloom Energy is one of them. Many arguments you’re already sufficiently familiar with.

The meaning is: You indeed have to go through thick and thin and keep calm, but at the end of the day, the investment pays off. Just look at the trends of the future, and commit to companies that have a leading technological role there and have a growth plan for good positioning in this new market. Bloom has acknowledged the signs of the times with its SOFC fuel cell systems and electrolyzers. With these, clean energy can be gotten – whether via natural gas, biogas or hydrogen. In addition, Bloom also possesses electrolysis knowhow and will itself be producing green hydrogen.

By 2026, Bloom wants to already be making 2.5 to 3 billion USD from sales. And by 2030, it is to be already 8 to 10 billion USD from FC systems alone. A global market on the order of 1.4 trillion USD. Furthermore, 7 to 10 billion USD more is to come through electrolysis, carbon capture technology and maritime applications – with an annual growth of altogether 30 to 35 percent. The gross profit margin Bloom sees at 30 percent and net profit margin at 15 percent.

“In all its businesses, Bloom Energy has a long growth runway. The company’s focus on growth, while keeping costs in check, bodes well for its long-term success, as well as the price of its stock.”

Motley Fool

MSC meanwhile plans to commission two cruise ships with hydrogen fuel cells. Investment sum: 3.5 billion USD. Maybe Bloom’s involved? Soon, Bloom is also building an FC power plant of 1 MW for luxury auto manufacturer Ferrari.

Summary

Bloom is well on the way to achieving the high targets it has set itself. Bloom has several big fantasies, which can be traced back to the technological successes of the company. It addresses the right markets and is receiving major support in many new markets from the Inflation Reduction Act. Major customer and shareholder SK ecoplant now needs to send the second tranche in the amount of 250 million USD out of the total investment of over 550 million USD.

Verdict: Any major dip as a result of profit-taking should be used for additional purchases, since the sustained goal of long-term high growth of 30 percent p. a. will also be reflected in the performance of the share price. Special developments might also come through big orders. My goal: 100 USD three years from now, 50 USD in 2023.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.