When you read these lines in the newest H2-international issue, clarity will have been provided. Actually, all of the figures for 2022 and the first quarter 2023 should have been presented before May 15, then the responsible committee of Nasdaq agreed to an extension, and the figures for 2022 and the Q1 2023 have now been submitted. Without going into detail, this is how the new executive board has cleared up the situation. Per the end of May, the company still has available 185 million USD in liquid capital.

A good position paper

Advertisements

At the trade fair Advanced Clean Transportation (ACT) Expo held at the beginning of May in Anaheim, California, Hyzon presented a new in-house-developed fuel cell design for trucks and additionally published a position paper titled “Designing the Future of Fuel Cells.” This involves a single 200-kW FC system different from systems put together from two or more 90- to 150-kW FC units. This “single stack” is intended to combine a variety of advantages:

– 30 percent reduction in volume

– 30 percent weight reduction

– 25 percent cost reduction of the stack

– 20 percent increase in travel range

These could be competitive advantages not to be underestimated, the managing director of Anleg, Jan Andreas, shared with H2-international.

Hyzon’s aim is to emerge stronger from the balance sheet crisis triggered by the previous management board and to be able to concentrate on its business with hydrogen-powered trucks. The stock market price must sustainably stay above the 1 USD mark, though, as prices of under 1 USD create the danger of a delisting or a change of stock exchange location. This entails the possibility of executing a reverse split of the shares in order to thus, via consolidation of the outstanding shares, force the price to over 1 USD. This would be a bad idea, though. As only about 30 percent of the shares are even freely traded, good news would quickly create room for higher share prices, especially since 20 percent of these freely tradable shares have been sold short (nearing 20 million in number).

That the major controlling shareholder Horizon from Singapore will take Hyzon off of the stock exchange seems unlikely, as they can generate further important capital of their own via the stock market simply through the issuance of more shares. Otherwise, the effort to continue to be listed on Nasdaq would also be superfluous. The company is an exciting turnaround and growth story for hydrogen in commercial vehicles all the same, even if certainly highly speculative, which is attributable to its status as a startup. Short sellers are still dictating the picture with nearly 20 million shares, but that can soon change. The share price is well hedged via liquidity (stock market value: 140 million USD), but achieving prices of over 1 USD is very important. The company now appears to be well positioned and, after all the past quarrels, can once again devote itself fully to the subject of hydrogen in the commercial vehicle sector.

Hyzon is expanding the core team: With the new COO Dr. Bappa Banerjee comes his comprehensive knowhow from many years in top management at companies like Caterpillar.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

The decline in the share price of Ballard Power in the past months is ascribed to the impatience of the many investors who assess primarily the short-term potential of this market leader in the PEM FC area. What counts is the long-term outlook of the company.

Current quarterly figures give credit to the skeptics. Ballard itself is not fighting this, as they are working unperturbed on the long-term strategy: establish production capacities, cooperations and pilot projects. This will be accompanied by capital outflows as well as the “logical” losses that it will entail. Ballard has enough capital in the bank to be able to implement the plans without outside pressure: 864 million USD in the bank account speaks for itself.

Advertisements

At the same time, Ballard is working on the constant optimization of its technologies, be it the MEA for the fuel cell, the FC modules, or the stacks for various applications, to be among the top suppliers on the market. But how will the stock market react when the production sites in China, Europe, the USA and Canada (eventually also in India – see Cummins with Tata) are utilized to capacity and then promise, in addition to high sales growth, a good profit?

China could be the wild card

Ballard president Randy McEwen is traveling for several weeks through China to meet with representatives of public authorities, ministries, companies, customers and municipalities as well as other players important for Ballard. This is certainly about understanding why China’s H2 support program has yet to be approved. The probably still largest FC stack production facility in the country – operated as a JV by Weichai and Ballard – is still “unemployed.”

That a larger program will come is, for me, no question, as many companies and regions or cities in China have now seized the topic in a variety of ways on their own (e.g. capacities for different electrolyzer types, stacks, vendor parts, FC trucks, H2 pipelines, refueling stations). For these is expected a high growth potential, which ought to be made use of. Perhaps China will still surprise the world with an H2 program in 2023 that not only matches, but makes the equivalent programs in the USA, Europe, Japan and elsewhere look smaller?

What would happen if China also gave passenger car fuel cells a boost with a national quota? China already did this for the battery– in the largest automotive market in the world – with the EV mandate, and all auto companies producing in the country have had to adapt to it. Ultimately, China has provided the foundations for battery-electric mobility worldwide.

By the year 2030, 1 million vehicles refuelable with hydrogen are to be running in China. Perhaps this goal will be adjusted against the South Koreans, since South Korea wants to be able to fuel over 6 million vehicles with hydrogen by 2040. For Ballard, a positive turnaround could come about very quickly from this, which would then also help the share price soar.

150 million kilometers clocked

Ballard meanwhile reports 150 million kilometers driven (93.2 million miles) by commercial vehicles and buses equipped with its technology – and smoothly. Worldwide, 3,800 buses are driving with Ballard inside. The Canadian company is setting an industry and sector standard with this. They are very well positioned in terms of total cost of ownership, according to CEO Randy McEwen.

“At Ballard, we are designing our PEM fuel cell engines for heavy-duty mobility applications where zero emissions, reliability, and durability are key differentiators for end-user total cost of ownership. We continue to set the industry benchmark for PEM fuel cell performance in our target markets. The accumulated distance driven by FCEVs powered by our technology underlines Ballard’s customer focus and commitment to reliable service and high uptime. We achieve this industry milestone at a time when we are seeing growing customer interest in the adoption of hydrogen fuel cells in our key mobility verticals of bus, truck, rail, and marine, as well as off-highway and stationary power applications.”

Randy McEwen, Ballard chief

First quarter has little predictive power

Order volume ended up good: 137.7 million USD, a doubling from the same period the previous year. Turnover for the quarter reached 13.3 million USD, which was below analysts’ expectations. Good things can be expected from the second half of the year. McEwen sees a very busy second half of 2023 and an excellent year 2024.

In the bus sector came three new OEMs, so companies that build buses and are relying on the FC module and knowhow from Ballard. Van Hool and Solaris have long been satisfied customers. Over 500 FC buses are currently set to be ordered in Europe, a large share of which equipped with Ballard. Meanwhile, 1,500 transit buses are in the tendering process – in Europe. For me, however, this is just an indicator of a development that will really pick up speed in the coming years.

The same pertains to commercial vehicles, where gradually the major truck manufacturers are turning, in addition to battery-electric solutions, to hydrogen. About this, McEwen said, “To be clear, the truck market is in the very early phases of fuel cell market adoption.” Here, Ballard is supplying stacks to various OEMs such as Quantron, and further customers may follow. In the area of trains, things are also slowly getting underway, which the rising orders of Ballard partners Stadler and Siemens Mobility show. Their customers are increasingly opting for a mix of battery-electric and hydrogen-powered trains. Ballard is also well positioned here – often in competition with Cummins or Alstom.

First Mode has raised its order for FC modules for heavy mining trucks from 30 to 35, and it’ll be likely 400 units in total for its partner Anglo American. For Canadian Pacific Rail (CP), locomotives have already been equipped with FC modules. Larger orders will probably come, and can be expected in the second half of the year.

In Norway, meanwhile, the ship MF Hydra was put into operation. Liquid hydrogen is turned into energy with the help of Ballard’s 200-kW module. The ferry for 300 people can travel for up to 21 days with it.

Everything out of pocket

The capital invest in the amount of 37.5 million USD in the first quarter mainly went into increased spending on R&D and product development – with over 860 million USD in the bank, not an issue. Interesting is an analyst’s question of why Ballard wants to allow new authorized capital to be given (so the possibility of issuing further shares), since it has sufficient liquidity at its disposal. This here is only about an extension of an expiring program or entitlement to issue further shares, so the tenor. They will also not make this a custom, was the answer.

I would interpret it differently: Ballard could quickly issue further shares if a takeover (acquisition) of a strategically interesting company presents itself, and quickly generate own capital through these shares or their equivalent, without having to dig into the high cash cushion. Everything has two sides.

Summary

Ballard may seem boring and is a big disappointment in terms of share price. The company has a very good standing, however, and is establishing and expanding its international presence, and is positioning itself so that it can in the future make and sell large numbers of stacks and modules for a variety of FC markets and thus earn money. As a partner of various OEMs, Ballard can Provide FC expertise and knowhow to a number of companies. These OEMs do not need to research and develop in this direction themselves: They buy turnkey products from Ballard and enter in competition with companies such as Toyota and leading truck manufacturers.

The China card would open up all possibilities should the country agree to a comprehensive H2 program, as Ballard would then be a big winner. Besides China, Ballard should also put its focus into India, which has a strong interest in hydrogen (see report on p. 58). Ballard equipped the first H2 train to run there. Thinking about the JV of Cummins and Tata Motors, Ballard could enter a similar venture with Ashok Leyland or Reliance. But that is only my personal view. Whoever sees Ballard in the medium or long term should use the severely depressed share prices for new and further buys.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

A look at the share prices of hydrogen and fuel cell companies, which have come under severe pressure, suggests that something is not right with the new megatrend hydrogen. What forces are at work here? Short sellers may have an influence, but ultimately it is the markets, the stock exchange and investors that determine the values. Also clear is: The real H2 ramp-up will gain speed in years, not months, and develop sustainably.

At this time, there are concrete projects worldwide to read of that today already correspond to a volume of 320 billion USD and will possibly reach 1 trillion USD per year. The snag is that so far only five to ten percent of these announced projects are in the approval or funding phase or, even, implementation.

Advertisements

Long-term upward trend is foreseeable

At the moment, companies are primarily concerned with positioning, establishing and scaling production, investing massively in research and development, and optimizing. Illustrative are the results and forecasts presented at important congresses such as at the recent World Hydrogen Summit in Rotterdam, at the newspaper-hosted summit Handelsblatt Wasserstoff-Gipfel in Salzgitter, or at Hannover Messe, which as an indicator for H2 and FC technologies, gives a perfect description of the situation.

Then, there are all the country-specific congresses, like the American Hydrogen Summit, which is representative of similar events around the globe. In parallel, numerous specialized events from the DVGW (German association for gas and water standards), Zukunft Gas and Mission Hydrogen for specific individual topics are taking place, which bodes optimism. Things are becoming optimized, researched, developed, and massive, truly gigantic new world markets are emerging to deal in energy security and likewise the issues of climate, the environment, and energy availability for all markets and uses concerned.

There is also criticism, however, with respect to the EU and Germany in particular, as many things are proceeding too hesitantly and the reasonableness of some regulations ought to be examined. Dr. Sopna Sury, executive at RWE Generation, stated at the Handelsblatt hydrogen summit: We’re simply acting and not waiting on politics. This attitude is illustrated at RWE Hydrogen with many individual projects such as an ammonia terminal in Brunsbüttel, but also in various applications of German electrolysis technology, like that of Sunfire, in Lingen.

All this shows: Countries and companies that approach the hydrogen market with many colors and in order to build businesses belong to the success of the ramp-up. Regarding investment in the H2 and FC stocks analyzed here, all of this sets the perfect runway for the companies concerned. Because their valuation and prospects are expressed in the prices of their shares and the performance of these at the stock market.

Current quotes will be quotes of opportunity

While all the companies and their shares discussed here have different valuation criteria, based off of the different business models, technologies and markets, what they all have in common is that they will play a role in and benefit from the new megatrend hydrogen. We are only at the beginning, though, and with every beginning also comes uncertainty. Here especially, as regeneratively produced hydrogen is a new world market.

You read correctly: Money is needed if you want to make use of the very strongly depressed prices for new or further buys. The basic conviction is that this megatrend talked of has only just begun, if trend research is taken as a basis. A megatrend needs 20 years until the breakout, the inflection point. Go back to the period from 2001 to 2003, when hydrogen and fuel cells started to increasingly come into the public eye. A Ballard Power share was priced at over 130 USD.

Take a seat on the H2 train: We have – metaphorically speaking – just left the station and the H2 train is now picking up speed. The pace is increasing, but the cruising speed has still not been reached. Remember the period from 2018 to 2020, when the share prices rose by several hundred percent but then went downhill for two years? Now, though, my opinion, the new trend will transition to a sustainable upward trend that will tend to lead, with fluctuations that are normal, to substantially higher prices for the shares here discussed. Do you already have your ticket for the H2 train?

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

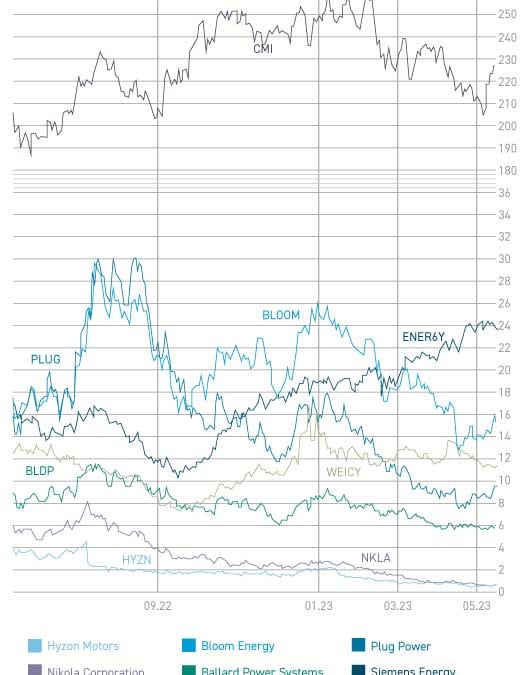

Written by Author Sven Jösting, June 9th, 2023 graph-7-23.jpg, Source: www.wallstreet-online.de

At the beginning of December 2022, Siqens appointed a new chief executive officer. Thomas Klaue made the move into management from the company’s advisory council where since 2019 he had represented the interests of Siqens’ founders. Klaue has relevant experience of capital market areas and has been working in various leadership posts at a range of organizations for over 15 years. His aim is to “replace today’s still widespread diesel generators with a carbon-neutral alternative” using the company’s own methanol-operated fuel cells. Co-founder Volker Harbusch, who previously ran the company single-handedly, will now concentrate his efforts on the technical side of the business as chief technology officer.

More than four billion tonnes of cement are produced worldwide every year. In the process, the building material inevitably releases large quantities of the carbon dioxide bound in the lime. Cement manufacturers, such as CEMEX from Mexico, are meeting the gigantic challenge of decarbonizing the industry. A bottleneck in the development is lack of green hydrogen. The building materials manufacturer has now set ambitious targets for itself. The site in Rüdersdorf is to serve as a blueprint.

For production of green cement, it is not only the required energy that is a problem, since only one-third of the CO2 emissions originate from the energy input. Two-thirds are intrinsic to the system. These are emissions that arise in the course of cement production itself. A cement produced with purely green energy still releases huge amounts of CO2 during the production process. Businesses and researchers want to change this.

Advertisements

Change for the climate also means changing cement to eco-cement. Various scientists are also working on this, among them the research institute Empa in Switzerland, which is developing a CO2-negative magnesium-based cement. Building materials manufacturer CEMEX also wants to rapidly reduce its emissions. According to the company’s calculation, it is already releasing 35 percent less CO2 than in 1990, Sergio Menendez states. He is president of CEMEX Europe, Middle East, Africa and Asia. By 2030, it should be 55 percent less in Europe, and the manufacturer wants to produce only CO2-neutral concrete worldwide by 2050.

So far, however, there has been little demand for green products, CEMEX speaker Alexandra Decker laments. The company therefore has the idea of separating carbon dioxide from exhaust gas, storing it temporarily and then converting it together with H2 into synthetic fuel. Thus providing a product that is planned for in advance and producible on demand. “This is another reason why we only want to use green hydrogen,” Decker assured H2-international.

CEMEX has specifically chosen to build electrolyzers at the location in Rüdersdorf so that it can supply the factory there with hydrogen from green electricity. In this way, H2 that might be needed for other industries would also not be taken off the market. The construction would have to start in 2025/26 for the site to produce CO2-free from 2030 onwards, Decker states.

The consortium Concrete Chemicals

In order to free not only cement production but also air traffic from CO2, three companies founded the project consortium Concrete Chemicals. CEMEX, with 56,000 employees worldwide and its own locations in Germany; Sasol ecoFT, a subsidiary of chemical corporation Sasol; and Uckermark-based Enertrag plan to produce a sustainable aviation fuel that can also be used in cement production. For this, a power-to-liquid method (PtL) will come into use. CO2 and H2 are converted into syngas. The mixture of carbon monoxide and H2 is then, with the aid of the Fischer-Tropsch process, converted into longer-chain hydrocarbons to produce e-kerosene.

The project in Rüdersdorf comprises two scaling levels. First, the hydrogen will be produced on site with electricity from regional renewable energy plants. In this first stage, 15,000 tonnes of e-kerosene are to be produced annually this way. For it, 100 tonnes of CO2 per day are to be captured in Rüdersdorf, combined with 12 tonnes of H2 per day and used for PtL production. In the second stage, larger quantities of H2 are to be delivered by pipeline.

The green hydrogen will be generated as part of the IPCEI project Elektrolyse-Korridor Ostdeutschland (electrolysis corridor Eastern Germany) to build a capacity of 210 MW. This will enable the production of 35,000 tonnes of e-kerosene per year. This project also uses only renewable electricity for the production of 40 tonnes of green hydrogen per day, the consortium states, which requires that another 300 tonnes of CO2 per day be sequestered.

The partner network Doing Hydrogen

Concrete Chemicals as well as Elektrolyse-Korridor Ostdeutschland are part of the IPCEI partnership project Doing Hydrogen. During construction of the pipeline from Rostock to Sachsen, all components of an H2 value chain will be covered. The resulting transmission system is to be built by 2026, two-thirds by conversion of existing natural gas infrastructure and one-third by the construction of new complementary hydrogen lines. In this way, a starter grid with a total length of 475 kilometers will arise that connects production and use points in Mecklenburg-Vorpommern, Brandenburg, Sachsen, Sachsen-Anhalt and Berlin.

The e-kerosene is then also to be certified for use in aircraft, since no alternative propulsion systems in the aviation sector are in sight for the foreseeable future. Through PtL, fuel of exactly the same specifications as petroleum-based kerosene can be created. With this, no modification of the existing drive technologies is needed. The three companies want to meet the criteria for aviation fuel set out in the EU directive RED II. Fuel having the prescribed minimum percent of PtL kerosene to be blended can be achieved this way.

The market for e-kerosene

The EU proposal ReFuelEU Aviation represents a first step towards the decarbonization of air transport. At the same time, it should ensure the purchase of synthetic fuels such as e-kerosene. At EU level, the regulation includes a sub-quota of 0.7 percent synthetic fuel out of the required quota of sustainable fuels for year 2030. The quota is to rise to a minimum of 28 percent e-fuels by 2050. “In this way, demand is plannable and ensured,” states Enertrag speaker Matthias Philippi.

Furthermore, under the German fuel blending regulation (Beimischungsverordnung), the fuel for all aircraft refueling in Germany will need to contain at least 0.5 percent PtL kerosene starting as early as 2026, and 2 percent starting 2030. This should increase the share of renewable energy in the transport sector to 28 percent by 2030.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.